This article is the final project submitted by the author as a part of his coursework in Executive Programme in Algorithmic Trading (EPAT™) at QuantInsti. Do check our Projects page and have a look at what our students are building.

About the Author

Harish Maranani is an EPATian. His educational qualifications include:

- Bachelors in Technology in Electronics and Communications Engineering from Acharya Nagarjuna University,

- MBA Finance from Staffordshire University (UK),

- Certificate in Quantitative Finance (CQF), and

- Master of Science in Mathematical and Computational Finance from New Jersey Institute of Technology, Newark, USA.

Harish was enrolled in the 27th Batch of EPAT™, and this report is part of his final project work.

Aim: To implement pairs trading/statistical arbitrage strategy in currencies.

Pairs Chosen: EURINR, USDINR, GBPINR, AUDINR, CADINR, JPYINR

Frequency: Daily

Time Period: 2011/4/21 to 2013/5/22

Implemented using: Python.

Pair Selection Criteria for FX Markets:

- The time series data for the above-chosen currency pairs is imported from quandl python api.

- Co-integration Test is carried out on all possible pair combinations viz. EURINR-USDINR, EURINR-GBPINR etc.

- Selecting Co-integrated pairs whose t-static value is less than 5% critical value of -2.8.

- Slicing the pairs which meet the co-integration condition for further analysis.

- To further test for confirmation of co-integration, CADF test is carried out on the sliced pairs from the pool.

- Z-score is calculated for each selected pair combination and the strategy is applied.

- Profit/loss, equity curve, maximum drawdown, are calculated/tabulated/plotted.

- Consider two currency pairs EUR/INR and USD/INR. Here the base currencies are EUR and USD respectively and the counter currency is INR.

Preliminary Test:

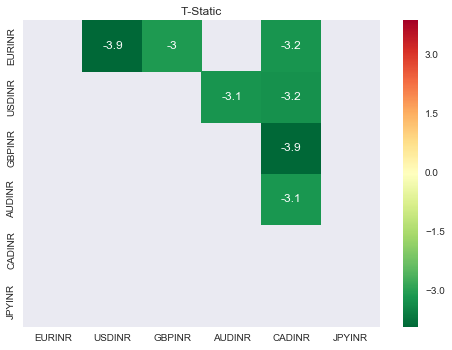

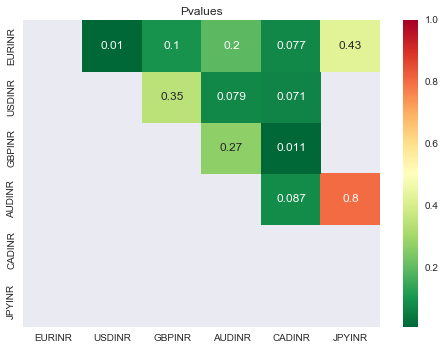

- In order to find the pairs of currencies that are co-integrated, a preliminary test through coint(x,y) from statsmodels.tsa.stattools is carried out and their respective pvalues, tstatic are plotted below.

- The t-static values that are displayed below are the ones that passed the co-integration test. i.e the t-static values smaller than the 5% critical value of -2.86.

Below is the list of pairs whose T-static values are less than the 5% critical value of -2.86:

- ['EURINR/USDINR: -3.89372142826',

- 'EURINR/GBPINR: -3.04457063111',

- 'EURINR/CADINR: -3.16044058632',

- 'USDINR/AUDINR: -3.14784526027',

- 'USDINR/CADINR: -3.19434173492',

- 'GBPINR/CADINR: -3.86588509209',

- 'AUDINR/CADINR: -3.10827352646']

Below is the plot of p-values of the co-integrated pairs:

Before rejecting null hypothesis to confirm the prices are mean-reverting, we shall conduct Co-Integrated Augmented Dickey-Fuller (CADF) test to confirm the same for the above sliced pairs out from the whole set of currencies. Below are the Results and plots.

We shall consider the 4 co-integrated pairs based on T-Static Values for CADF testing.

The following are the 4 Co-integrated pairs:

EURINR/USDINR: -3.89372142826

GBPINR/CADINR: -3.86588509209

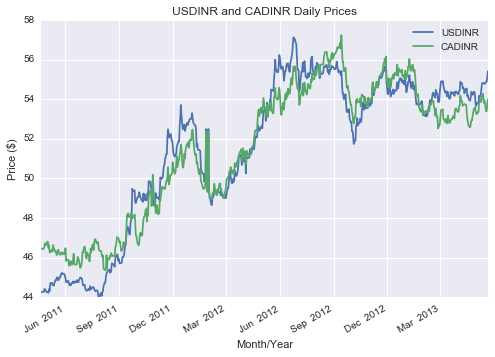

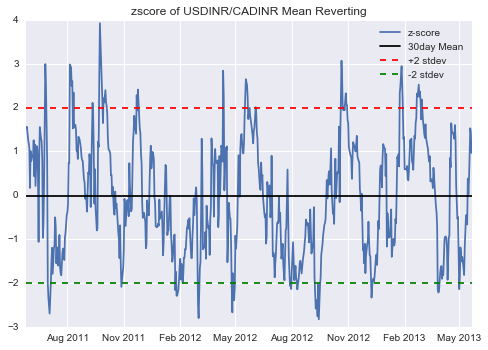

USDINR/CADINR: -3.19434173492

EURINR/CADINR: -3.16044058632

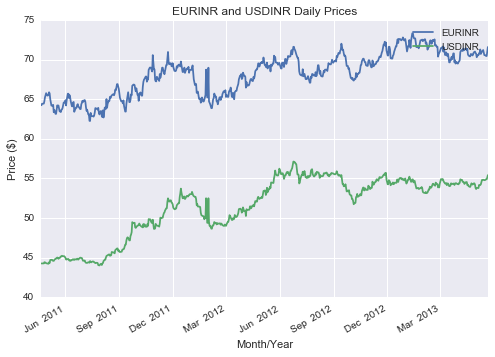

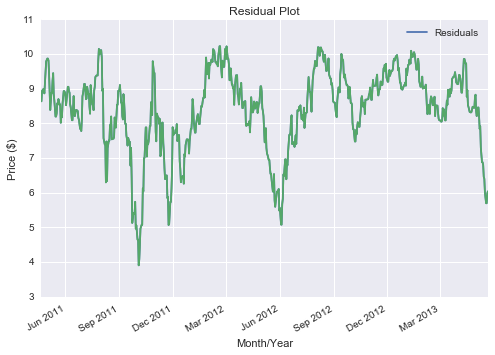

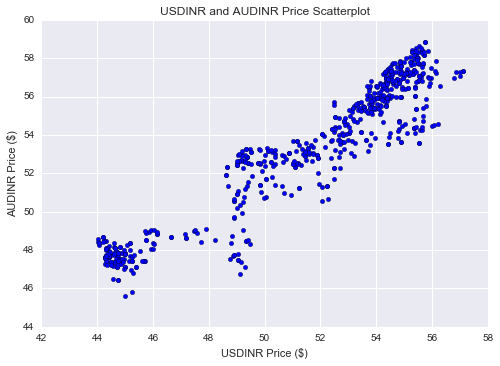

EURINR/USDINR

TIME SERIES PLOTS OF EURINR/USDINR

From the above graph, it is visibly evident that the prices are co-integrated, however, to statistically confirm the same, the below set of tests/procedures are implemented.

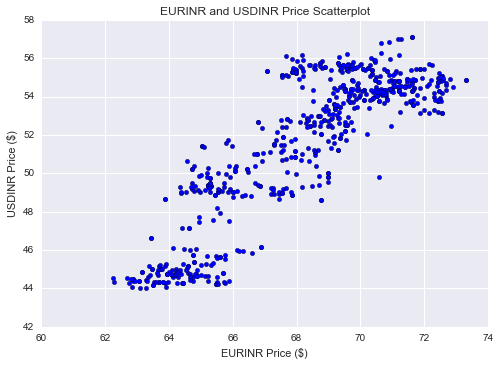

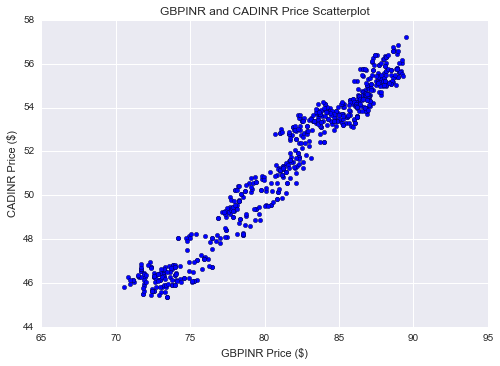

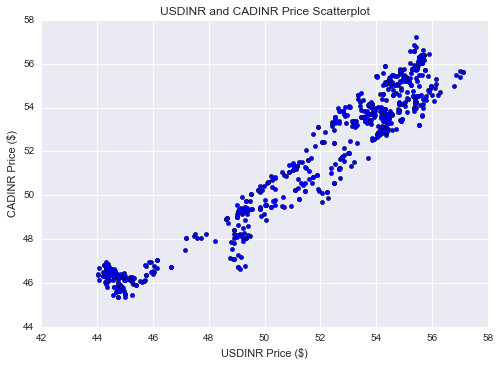

Creating a scatter plot of the prices, to see the relationship is broadly linear.

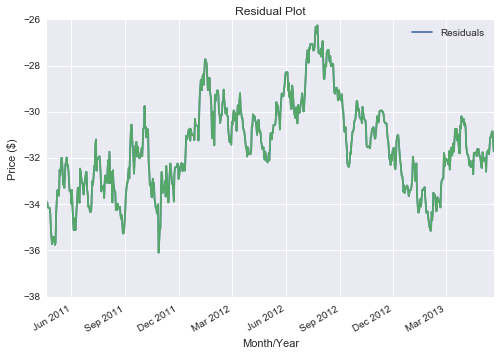

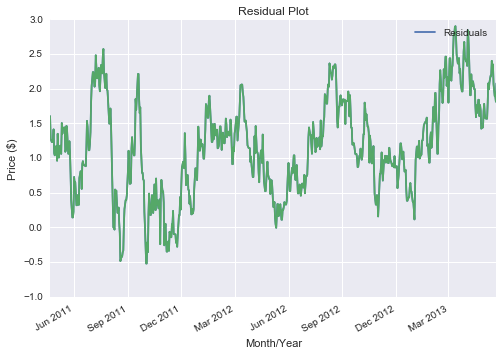

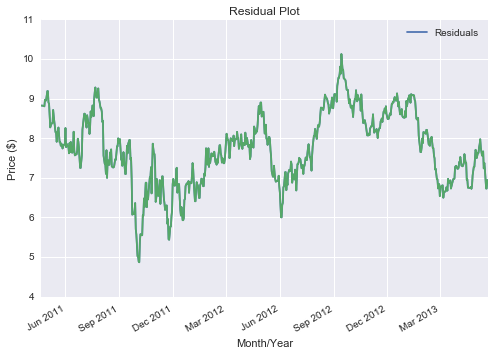

Given the above residual plot, it is relatively stationary.

Co-integrated Augmented Dickey-Fuller Test Results

Co-integrated Augmented Dickey-Fuller (CADF) test determines the optimal hedge ratio by performing a linear regression against the two-time series and then tests for stationarity under the linear combination.

Implementing in python gives the following result:

(-3.0420602182962395,

0.03114885626164075,

1L,

652L,

{'1%': -3.440419374623044,

'10%': -2.5691361169972526,

'5%': -2.8659830798370352},

852.99818965061797)

Given the above results, the t-static to be -3.04 less than 5% critical value of -2.8, we can reject the null hypothesis and can confirm that the prices are mean-reverting.

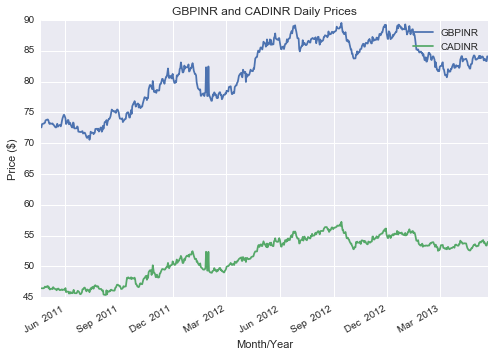

GBPINR/CADINR

Below are the time series, scatter and residual plots of GBPINR/CADINR

CADF Test results:

(-3.3637522231183872,

0.012258395060108089,

2L,

651L,

{'1%': -3.440434903803665,

'10%': -2.569139761751388,

'5%': -2.865989920612213},

-179.04749802146216)

Given the above results, the t-static to be -3.36 smaller than 5% critical value of -2.8, we can reject the null hypothesis and can confirm that the prices are mean-reverting.

USDINR/CADINR

CADF Test results

Given the above results, the t-static to be -2.93 smaller than 5% critical value of -2.8, we can reject the null hypothesis and can confirm that the prices are mean-reverting.

(-2.9344605252608607,

0.041484961304201866,

1L,

652L,

{'1%': -3.440419374623044,

'10%': -2.5691361169972526,

'5%': -2.8659830798370352},

-99.577663481220952)

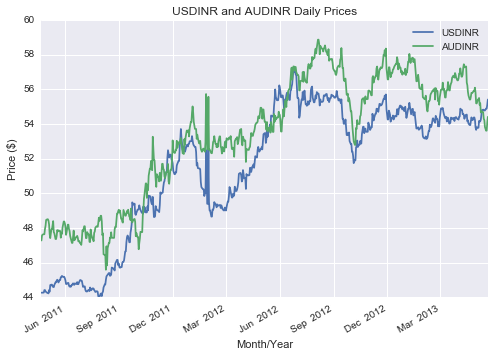

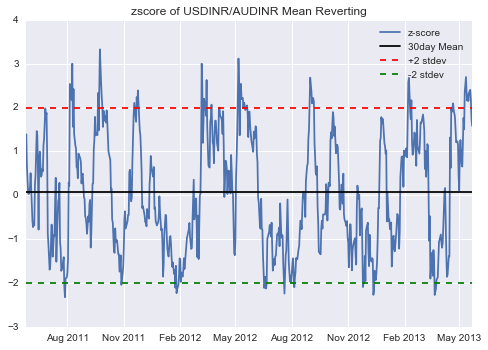

USDINR/AUDINR

Below are the results from CADF test:

(-3.2595055880757768,

0.016788501512565262,

4L,

649L,

{'1%': -3.440466106307706,

'10%': -2.5691470850496558,

'5%': -2.8660036655537744},

381.77145926378489)

With the t-static value of -3.25 smaller than the 5% critical value of -2.86, we can reject the null hypothesis and can confirm that the pair is co-integrating.

Now that we have found the co-integrated pairs in the form of following pairs with t-static values:

- EURINR/USDINR: -3.04

- GBPINR/CADINR: -3.363

- USDINR/CADINR: -2.934

- USDINR/AUDINR: -3.259

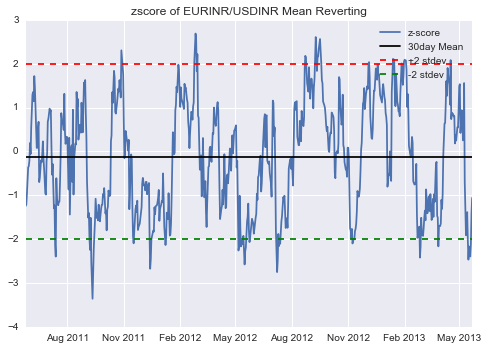

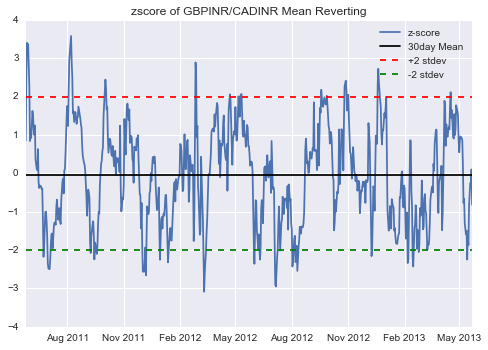

Next Step would be to calculate the Z-score of the price ratio for 30day moving average and 30day standard deviation:

- Calculating price ratios and creating a new column ratio in the data frames (df, df1, df2, df4) of the above currency pairs respectively.

Below is the snapshot of the data frames:

df:

Df1:

Calculation of Z-score of the price ratio for the 30-day window of moving average and standard deviation:

- Below are the plots of z-scores for the above co-integrated pairs with their respective price ratios:

From the above Z-Score plots of the selected pairs, Z-score is exhibiting mean reverting behavior within 2 standard deviations.

Building a Trading Strategy:

- When z-score touches +2 short the pair and close the position when it reverts back to +1

- When z-score touches -2 long the pair and close the position when it reverts back to -1.

- Only one position is held at a single instance of time.

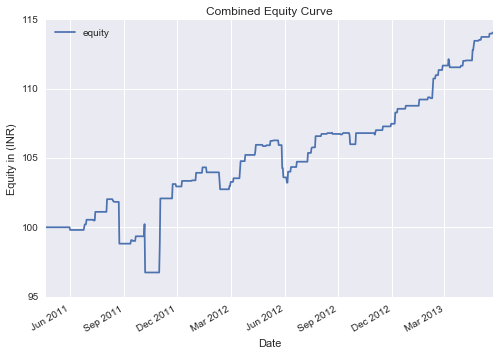

Equity Curve:

Plotting the equity curve with the starting capital of 100 INR equally divided among 4 pairs.

With 100 INR initial Capital, equity ended at 114.05.

Cumulative profit to be 14% without any leverage. With 10 times leverage (ideal for FX trading), the profits can be seen at 140%. Below are the important performance metrics of the strategy.

| Profit percentage Without Leverage | 14.0514144897 % |

| Profit percentage with 10 times leverage | 140.514144897 % |

| Number of Positive Trades | 59 |

| Number of Negative Trades | 23 |

| Hit Ratio | 71.9512195122 % |

| Average Positive Trade | 0.46886657456220338 |

| Average Negative Trade | -0.59181362649660851 |

| Average Profit/Average Loss | 0.792253766338 |

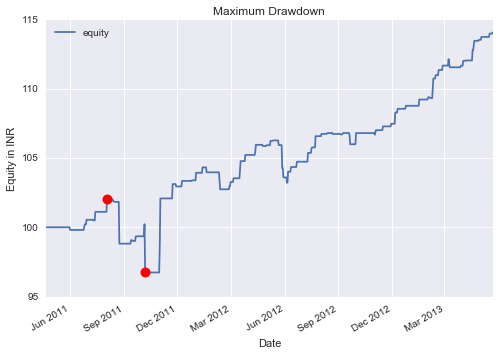

| Maximum Drawdown | -5.1832506579 % |

The above graph shows the maximum drawdown points marked with red dots and the value is added in the above table.

Instructions for Implementation

- Please run the IPython notebook named harish_stat_arb.ipynb for the confirmation of results and plots.

- Another option is to run the python script harish_quantinsti_final_project_code.py on any python IDE to confirm the results and graph.

- Use the below code for exporting the final dataframe to an excel file.

writer = pd.ExcelWriter('pairs_final.xlsx',engine = 'xlsxwriter')

pairs.to_excel(writer,'Sheet5')

writer.save()

Conclusion

Though the strategy has generated 140% returns over the backtest period of 2 years, the following factors should be considered in order to evaluate a more accurate performance of the strategy.

- The model has ignored the slippage and commissions

- The model ignored the bid-ask spread while placing buy or sell orders

Read about other strategies in this article on Algorithmic Trading Strategy Paradigms. If you also want to learn more, you can explore our Automated Trading Course here.

Bibliography

- Statistical Arbitrage lecture Quantinsti, Nitesh Khandelwal

- Pairs Trading, Ganapathy Vidyamurthy, Wiley Finance

- Successful Algorithmic trading, Michael Halls-Moore