By Lamarcus Coleman

In this post, we will create an intraday momentum strategy and use QDA as a means of optimizing our strategy. We'll begin by reviewing Linear Discriminant Analysis or LDA and how it is associated with QDA, gain an understanding of QDA and when we might implement this technique instead of Linear Discriminant Analysis. We will then create our intraday momentum strategy using data on the eMini S&P 500 futures and apply our QDA analysis to it to improve our trading strategy.

Let's get started!

Linear Discriminant Analysis Review

Recall that the purpose of using machine learning techniques is so that we are able to make better inferences and predictions from our data. Thus, the intent of machine learning is analogous to that of implementing a quantitative trading workflow. In quantitative trading, our goal is to eliminate cognitive biases toward the end of basing our decisions on sound evidence or logic. In other words, our aim is to remove and replace the subjectivity inherent in manual trading with objectivity offered via quantitative trading. Machine learning is a means to achieve this.

Classification is one type of machine learning problem. In a standard classification problem, we have some y or response that contains k levels or possible classes. We can use quantitative or numerical, qualitative or categorical, or a mix of the two data types as our X, or features to predict the class of our data.

In a trading context, an example of a classification problem is attempting to predict the direction of the next price. In a regression setting, we would attempt to construct a model that would allow us to predict the actual price or numerical response. So regression problems deal with numerical predictions and classification deals with categorical predictions.

When we implement a machine learning algorithm, we are making an approximation of f(x) which is an equation that represents the relationship between X or our predictors and y, our response. Parametric models offer us the advantage of focusing on estimating specific coefficients of an equation rather than estimating the entire equation.

This means that instead of trying to compose an entire equation that represents the relationship between our inputs and outputs, we can make some assumptions about our data and structure our model based on an existing equation and solve for the coefficients of that equation. There are pros and cons to such models which we won't go deeply into, but essentially, a model, in order to be effective in providing predictions, needs to reflect or "model" the data in reality. Models have inherent assumptions and if those assumptions are not consistent with reality, the model will have a low accuracy or predictive ability.

Given its name, you might have guessed that LDA assumes linearity.

In LDA we begin with k classes that our observations can fall into. The model creates a probability distribution for each k class. Unlike Logistic Regression which estimates the probability of an observation being in a specific class directly, LDA uses Bayes Theorem and sorta estimates this posterior probability indirectly.

For example, recall from algebra that the equation for a line is y=mx+b.

With this equation in hand, we can fit a line to our data simply by estimating m and b, where m is the slope or derivative(i.e. rate of change) of y given a one unit change in x and b is the intercept, or the value of y when x is equal to 0. This equation allows us, given some x values, to estimate the coefficients m and b, and make predictions for y.

This process is similar to that of implementing a parametric model. We have an assumption about how our data is structured, illustrated via our linear equation, and thus we can simply estimate our coefficients to make a prediction.

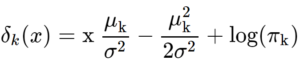

The equation for LDA is below:

In this equation, we are seeking to estimate μ or the mean of each k class, πk, or the prior probability of the kth class and σ2, or the common covariance matrix between each of the k classes. Once we have these coefficients, we can plug them into our equation to make our predictions.

We will cover more about LDA in our upcoming post which will be entitled "Using Linear Discriminant Analysis for Quantitative Portfolio Management." This post will be live soon.

What is Quadratic Discriminant Analysis?

Quadratic Discriminant Analysis is another machine learning classification technique. Like, LDA, it seeks to estimate some coefficients, plug those coefficients into an equation as means of making predictions. LDA and QDA are actually quite similar. Both assume that the k classes can be drawn from Gaussian Distributions. QDA, again like LDA, uses Baye's Theorem to estimate the parameters of the equation. The equation for QDA is below:

![]()

which equals:

![]()

So we can see that our QDA equation looks somewhat similar to that of our LDA equation, except that in LDA we estimate μk, πk and σ2, but in QDA we estimate μk, πk, and ∑k.

In LDA, we assume that each kth class has a shared covariance matrix, σ2. But in QDA, this assumption has changed and we now assume that each kth class has its own covariance matrix, ∑k.

Okay, by now you may be thinking, if there are similarities between LDA and QDA, why would we use QDA. Couldn't we just stick to LDA because it's quite obvious that QDA is a bit more involved and incorporates matrix multiplication?

Although LDA and QDA are similar, there exist instances where QDA should be used and may outperform LDA and vice versa. For example, LDA assumes that the k classes share a covariance matrix. If this assumption is invalid, then QDA will outperform LDA. Another consideration of the models is their flexibility. The flexibility of a model can be directly translated into a bias-variance tradeoff. The more flexible a model is, the more likely it is to overfit the data and have low bias but high variance. In contrast, the less flexible a model is, the more likely it is to have a high bias but low variance, and thus not really resemble the true population.

LDA is a lot less flexible than QDA. LDA will have a high bias, or not be representative of reality if the assumption of a common covariance matrix is incorrect. If this assumption is correct, it may be better to use LDA for classification versus that of QDA.

Also, the number of features plays an important role in model selection. If there are a lot of predictors, using QDA will be more computationally inefficient than that of LDA. This is because in QDA, you have more parameters to estimate and naturally this grows at some rate based on the number of predictors. QDA may be a better choice if there are a lot of training observations.

Intraday Momentum Strategy Development

Okay. Now that we've reviewed LDA and QDA, let's lay out the framework for developing our intraday momentum strategy. We will use intraday data for the eMini S&P 500 and apply the RSI as our indicator of momentum trading. Our goal is to construct our strategy, assess its performance, and then improve the performance of our strategy by using Quadratic Discriminant Analysis.

Let's import some of our usual libraries.

#data analysis and manipulation

import numpy as np

import pandas as pd

#data visualization

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')Now that we have our initial libraries imported, let's import our data. We will use pandas to read our data in as a csv file.

#initializing our data variable as our eMini data

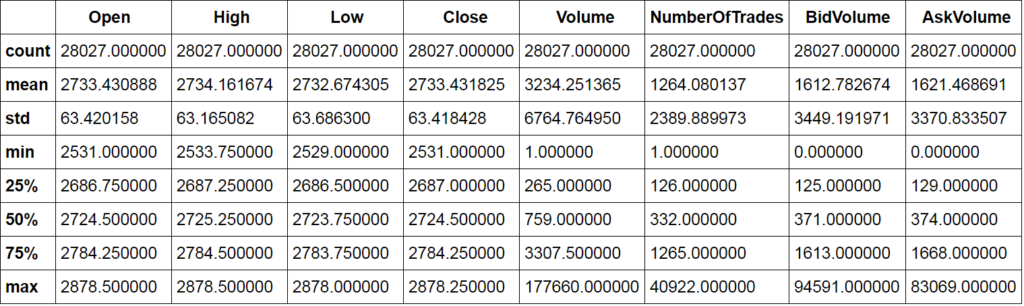

data=pd.read_csv('ESPostData.csv')Now that we have our data, let's do some exploratory data analysis on it. We'll start by using the info and describe methods and checking the head of our data.

data.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 28027 entries, 0 to 28026 Data columns (total 10 columns): Date 28027 non-null object Time 28027 non-null object Open 28027 non-null float64 High 28027 non-null float64 Low 28027 non-null float64 Close 28027 non-null float64 Volume 28027 non-null int64 NumberOfTrades 28027 non-null int64 BidVolume 28027 non-null int64 AskVolume 28027 non-null int64 dtypes: float64(4), int64(4), object(2) memory usage: 2.1+ MB

From applying this method, we can see the types of data in our dataframe as well as the columns. Let's now call the described method on our data.

data.describe()

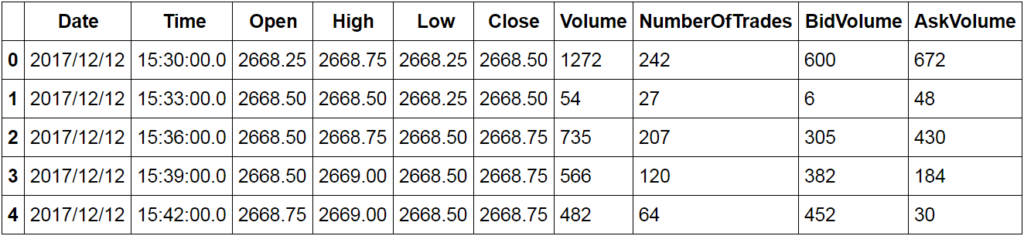

This method gives us some statistical information about our data. We can now check the head of our data.

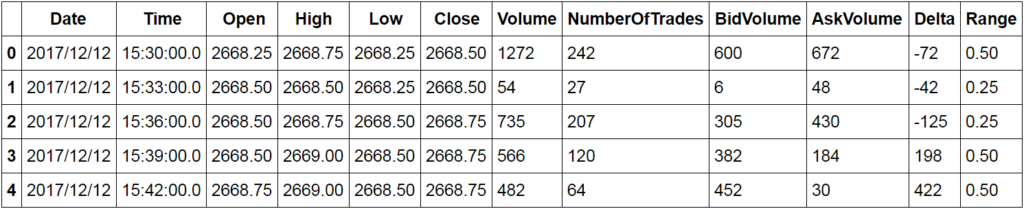

data.head()

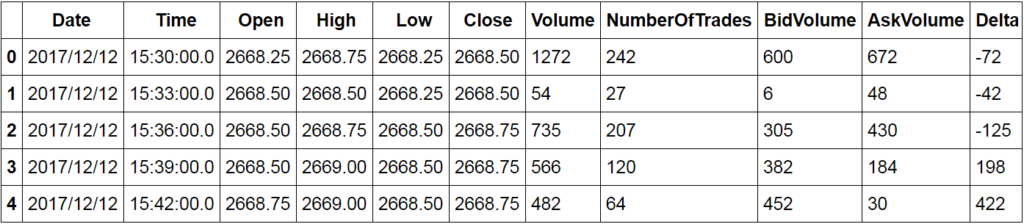

We're going to create a momentum based strategy. We can see that we have data for every 3-minute interval. The volume traded into the bid and the ask may provide some insight into short-term momentum. Let's create a delta column, our bid volume minus our ask volume, and compare this to the closing price and see if there is some relationship. We'll first make a copy of our data and then add our delta column.

#making copy of our data es=data.copy() #creating delta column es['Delta']=es[' BidVolume']-es[' AskVolume']

Now let's recheck the head of our data and create a regression plot.

es.head()

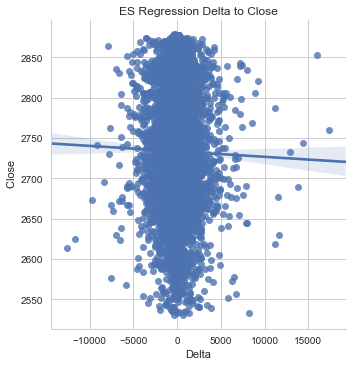

#creating regression plot

sns.lmplot('Delta',' Close',data=es)

plt.title('ES Regression Delta to Close')<matplotlib.text.Text at 0x16b7bae3080>

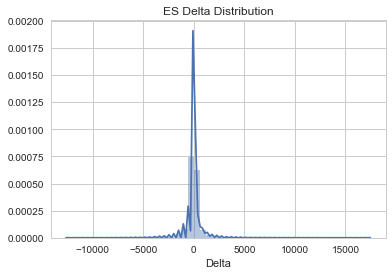

Now that we've gotten an idea of the relationship between our delta and closing prices, let's plot a distribution of our delta.

#creating distribution of delta

sns.distplot(es['Delta'])

plt.title('ES Delta Distribution')<matplotlib.text.Text at 0x16b7bbb3550>

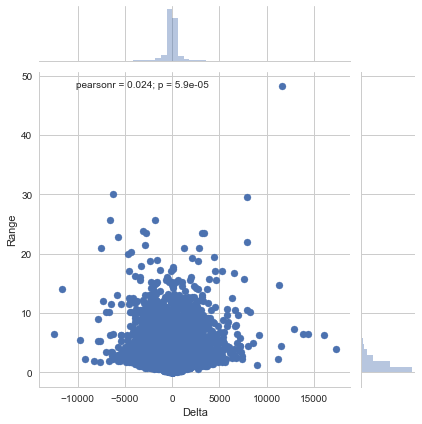

Now we'll add a range column to our data and view the relationship between the range of each bar and the delta.

#adding our range column es['Range']=es[' High']-es[' Low']

#rechecking the head of our data es.head()

Now we can create a scatter plot of our delta and the range of our data.

sns.jointplot(es['Delta'], es['Range'])

<seaborn.axisgrid.JointGrid at 0x16b7ee09470>

Now let's take a look at the distribution of the number of trades per bar.

#creating number of trades distribution sns.distplot(es[' NumberOfTrades'],bins=100)

<matplotlib.axes._subplots.AxesSubplot at 0x16b7ef2bc18>

Now that we've gained some insight into our data from our exploratory data analysis, we're ready to create our intraday momentum strategy using the RSI indicator. We'll wrap our strategy in a class which allows us to create different instances of our strategy without having to rewrite the same logic.

class rsi_strategy(object):

def __init__(self,data,n,data_name,start,end):

self.data=data #the dataframe

self.n=n #the moving average

self.data_name=data_name #the name that will appear on plots

self.start=start #the beginning date of the sample period

self.end=end #the ending date of the sample period

def generate_signals(self):

delta=self.data[' Close'].diff()

dUp,dDown=delta.copy(),delta.copy()

dUp[dUp<0]=0

dDown[dDown>0]=0

RolUp=dUp.rolling(self.n).mean()

RolDown=dDown.rolling(self.n).mean()

#assigning indicator to the dataframe

self.data['RSI']=np.where(RolDown!=0, RolUp/RolDown,1)

self.data['RSI_Slow']=self.data['RSI'].rolling(self.n).mean()

#creating signals

self.data=self.data.assign(Signal=pd.Series(np.zeros(len(self.data))).values)

self.data.loc[self.data['RSI']<self.data['RSI_Slow'],'Signal']=1

self.data.loc[self.data['RSI']>self.data['RSI_Slow'], 'Signal']=-1

return

def plot_performance(self,allocation):

#intializing a variable for initial allocation

#to be used to create equity curve

self.allocation=allocation

#creating returns and portfolio value series

self.data['Return']=np.log(self.data[' Close']/self.data[' Close'].shift(1))

self.data['S_Return']=self.data['Signal'].shift(1)*self.data['Return']

self.data['Market_Return']=self.data['Return'].expanding().sum()

self.data['Strategy_Return']=self.data['S_Return'].expanding().sum()

self.data['Portfolio Value']=((self.data['Strategy_Return']+1)*self.allocation)

#creating metrics

self.data['Wins']=np.where(self.data['S_Return'] > 0,1,0)

self.data['Losses']=np.where(self.data['S_Return']<0,1,0)

self.data['Total Wins']=self.data['Wins'].sum()

self.data['Total Losses']=self.data['Losses'].sum()

self.data['Total Trades']=self.data['Total Wins'][0]+self.data['Total Losses'][0]

self.data['Hit Ratio']=round(self.data['Total Wins']/self.data['Total Losses'],2)

self.data['Win Pct']=round(self.data['Total Wins']/self.data['Total Trades'],2)

self.data['Loss Pct']=round(self.data['Total Losses']/self.data['Total Trades'],2)

#Plotting the Performance of the RSI Strategy

plt.plot(self.data['Market_Return'],color='black', label='Market Returns')

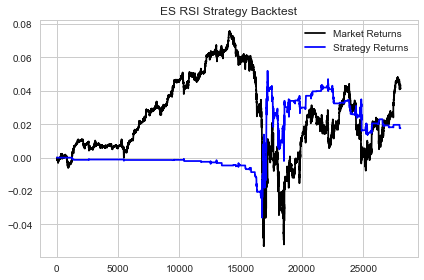

plt.plot(self.data['Strategy_Return'],color='blue', label= 'Strategy Returns')

plt.title('%s RSI Strategy Backtest'%(self.data_name))

plt.legend(loc=0)

plt.tight_layout()

plt.show()

plt.plot(self.data['Portfolio Value'])

plt.title('%s Portfolio Value'%(self.data_name))

plt.show()Okay. Now let's try out our rsi_strategy class.

#creating an instance of our strategy class strat1=rsi_strategy(es,10,'ES',es['Date'][0],es['Date'].iloc[-1])

Now that we have an instance of our RSI strategy, we can now call our generate signals and plot performance methods to see how our strategy performed.

#generating signals strat1.generate_signals()

#plotting performance of our strat1 strategy #passing in an allocation amount of $10,000 strat1.plot_performance(10000)

Now that we have built our strategy, we can check some of its metrics using functionality that we coded into our strategy class. We'll check our Hit Ratio, Win Percentage, and Loss Percentage.

#checking our Hit Ratio strat1.data['Hit Ratio'][0]

0.93000000000000005

This Hit Ratio shows us that our strategy currently has less than a 1-to-1 ratio between wins and losses. Let's now check our Win and Loss Percentages.

#checking our win percentage

print('Strategy Win Percentage')

strat1.data['Win Pct'][0]Strategy Win Percentage 0.47999999999999998

#checking our loss percentage

print('Strategy Loss Percentage')

strat1.data['Loss Pct'][0]Strategy Loss Percentage 0.52000000000000002

We can also check our total number of wins and losses as well as the total number of trades our strategy took.

#checking total number of wins strat1.data['Total Wins'][0]

10818

#checking total number of losses strat1.data['Total Losses'][0]

11613

#checking total number of trades strat1.data['Total Trades'][0]

22431

At this point, we've conducted exploratory data analysis on our data, created our intraday momentum strategy and viewed the metrics of our strategy. Our strategy currently has a Hit Ratio of little less than 1. Our win percentage is approximately 48% and our loss percentage is 52%. At face value, this isn't very impressive.

How can we improve our strategy so that we can actually profit from it?

Even though we tend to lose slightly more than we win, if we can effectively eliminate some of our losing trades, we can in-turn recalibrate our win/loss percentages and hit ratio. In other words, our winning trades aren't the problem. It's actually better to win 48% of the time than to win some amount less than 48% of the time. The problem is that given the distribution of our total trades, we don't win enough. What if we were to virtually eliminate all of our losing trades? We would trade a lot less, but our win percentage would skyrocket and thus allow us to trade our strategy profitably.

Properly identifying the problem or task is a key skill in any machine learning application. We will use QDA to improve upon our existing strategy. Our objective is to be able to predict when our strategy is likely to take a losing trade before it takes it so that we can eliminate losing trades and thus rebalance our win-loss percentages back in our favour. Sounds interesting! Let's get to it!

Optimizing The Intraday Momentum Strategy Using QDA

Now we will use QDA as a means of improving our intraday momentum strategy. Let's start by importing the necessary libraries from sklearn.

from sklearn.discriminant_analysis import QuadraticDiscriminantAnalysis from sklearn.metrics import confusion_matrix, classification_report

We need a way to determine when we are likely to place a losing trade. Hmmm… How about we add a categorical return column to our data. We can then do a bit of feature engineering and use our QDA classifier to predict the categorical return values. Once we've completed this, we can then test out our idea by feeding our strategy our predictions and seeing if this improves the performance of our strategy.

We'll start by making a copy of our strategy dataframe. Recall, this is the dataframe created when we built the initial implementation of our strategy.

df=strat1.data

Let's check the head of our dataframe.

df.head()

Now let's add our categorial return column.

#adding column to hold the direction of returns df['Return Direction']=np.where(df['Strategy_Return']>0,'Up',np.where(df['Strategy_Return']<0,'Down',"Flat"))

Let's call our head and tail methods on our Return Direction column.

df['Return Direction'].head()

0 Flat 1 Flat 2 Flat 3 Flat 4 Flat Name: Return Direction, dtype: object

df['Return Direction'].tail()

28022 Down 28023 Down 28024 Down 28025 Down 28026 Down Name: Return Direction, dtype: object

Now that we have added the Return Direction column we can begin thinking about what features we should use to predict the probability of our strategy making losses. We can use the volatility of the underlying as it should have some effect on our strategy. We could also use different lags of volatility to capture the evolution of momentum. We can also use our RSI indicator. Okay. Let's go with these and add them to our dataframe.

You may be wondering why we aren't using our signal generator. We want to train our model in a way that we can apply it to any market environment. At any given time, under a variety of market conditions, our longs and shorts could be distributed differently. For example, if we're in a bull market, we're more likely to get longer than short signals. We're also more likely to have a greater degree of profitability on our long trades versus our short trades. If we train our model to predict our losing trades on our signal generator over this period, it will associate long signals with increasing returns and short signals with decreasing returns. While this may be true at the moment, in the future when we enter a bear market, the model will have high bias and not be predictive of our losing trades.

#adding our features #creating volatility strat1.data['Vol']=strat1.data[' Close'].rolling(window=5).std() #creating lags of volatility strat1.data['Vol Lag 3']=strat1.data['Vol'].shift(3) strat1.data['Vol Lag 4']=strat1.data['Vol'].shift(4) strat1.data['Vol Lag 5']=strat1.data['Vol'].shift(5)

Okay, let's pause for a second and make sure we understand what's happening here. We began by conducting some exploratory data analysis on our intraday data. Our goal was to create an intraday trading strategy using the RSI indicator. We built a class that allowed us to create an instance of our momentum strategy. We weren't so thrilled about our strategy's performance but we did recognize that it had some potential.

Our strategy currently has a win/loss ratio of just under 1. It currently wins 48% of the time and loses 52% of the time. Our premise is that if we can eliminate some of our losing trades, and thus reduce some of the trades that we take, we could shift the probability of our strategy being profitable in our favour. The fact that we only win 48% of the time is not the real issue. If we could only take those trades, while we would cut our total trades in half, we would have a perfect (theoretically) strategy. In other words, we need a quantitative way of improving our strategy so that it can actually be used in production.

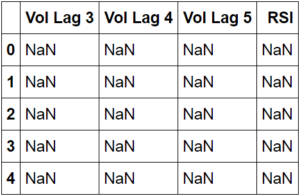

In order to achieve our goal, we must be able to predict when our strategy is likely to take a trade that is probable of making a loss. Thus, we created the Return Direction column to track whether we had a win or a losing trade. We needed features that we could use in our model for training that could provide some indication of the probability of losing trades. We chose volatility lags and our RSI and in the above block of code, we added volatility and its lags. Notice that we did this on "strat1.data" instead of our "es" dataframe. strat1.data is the dataframe that we created when we made the strat1 instance of our momentum strategy. We're simply calling the "data" dataframe that was created within our class and storing our features in it. The purpose of doing this is because we are optimizing our strat1 momentum strategy which holds our returns. Recall our es dataframe only holds the data that we passed into our strategy.

Once we create our QDA model, we can store its predictions in a copy of our es dataframe and then create a second momentum strategy instance and compare the results. We will need to alter our class a bit so that it will read our predictions before it takes a trade. So essentially, our strategy will only trade when our QDA model predicts that the trade is not likely to be a losing trade.

Now that we have our features, we can initialize our X and y variables and conduct our train test split. Let's make a copy of our strat1.data dataframe and check its head.

#copying our strategy dataframe df=strat1.data.copy()

#checking the head of our df dataframe df.head()

To ensure that we use all the appropriate columns, let's call the info method on our dataframe.

df.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 28027 entries, 0 to 28026 Data columns (total 33 columns): Date 28027 non-null object Time 28027 non-null object Open 28027 non-null float64 High 28027 non-null float64 Low 28027 non-null float64 Close 28027 non-null float64 Volume 28027 non-null int64 NumberOfTrades 28027 non-null int64 BidVolume 28027 non-null int64 AskVolume 28027 non-null int64 Delta 28027 non-null int64 Range 28027 non-null float64 RSI 28017 non-null float64 RSI_Slow 28008 non-null float64 Signal 28027 non-null float64 Return 28026 non-null float64 S_Return 28026 non-null float64 Market_Return 28026 non-null float64 Strategy_Return 28026 non-null float64 Portfolio Value 28026 non-null float64 Wins 28027 non-null int32 Losses 28027 non-null int32 Total Wins 28027 non-null int64 Total Losses 28027 non-null int64 Total Trades 28027 non-null int64 Hit Ratio 28027 non-null float64 Win Pct 28027 non-null float64 Loss Pct 28027 non-null float64 Return Direction 28027 non-null object Vol 28023 non-null float64 Vol Lag 3 28020 non-null float64 Vol Lag 4 28019 non-null float64 Vol Lag 5 28018 non-null float64 dtypes: float64(20), int32(2), int64(8), object(3) memory usage: 6.8+ MB

Now we can clearly see all of our columns. Our X or features will be our lags of volatility and RSI and our y or response will be our return direction column. We can now initialize our variables.

#initializing features X=df[['Vol Lag 3','Vol Lag 4','Vol Lag 5', 'RSI']]

#initialing our response y=df['Return Direction']

#checking the head of our features X.head()

We can now split our data into training and testing sets. We'll import traintestsplit from sklearn to do this.

from sklearn.model_selection import train_test_split

Now we're ready to use our traintestsplit method.

#initializing training and testing variables X_train,X_test,y_train,y_test=train_test_split(X,y,test_size=0.2)

Now that we have split our data into an 80/20 train test split, we can initialize our QDA model and fit it to our data.

model=QuadraticDiscriminantAnalysis()

Before we fit our training data, we'll need to fill the null values.

#fitting model to our training data #and filling null values with 0 model.fit(X_train.fillna(0),y_train)

QuadraticDiscriminantAnalysis(priors=None, reg_param=0.0, store_covariances=False, tol=0.0001)

Now that we have fitted our model, we can use it to make predictions by passing in our Xtest data. This data are our features that our model hasn't seen yet. We can then compare the predictions made by our model to the ytest data, or the actual values of our responses.

#creating predictions predictions=model.predict(X_test.fillna(0))

Now we will use our confusion matrix and classification report to assess how well our model did.

#initializing confusion matrix

print('Confusion Matrix:')

print(confusion_matrix(y_test,predictions))Confusion Matrix: [[4902 6 242] [ 2 0 0] [ 399 0 55]]

#initializing classification report

print('Classification Report')

print(classification_report(y_test,predictions))Classification Report

precision recall f1-score support

Down 0.92 0.95 0.94 5150

Flat 0.00 0.00 0.00 2

Up 0.19 0.12 0.15 454

avg / total 0.86 0.88 0.87 5606Wow! Our model is able to predict losing trades at an accuracy of 92%.

We can now add our predictions back to our es dataframe and then pass it back to our rsi_strategy class to create a strat2 instance and compare our metrics to our strat1 metrics.

Before adding our predictions to our es dataframe, let's recheck it. We'll call the head method on our dataframe.

#rechecking the head of our es data es.head()

Now let's add our predictions to our es dataframe.

Recall that in order to build our QDA model, we had to do an 80-20 train test split. This means that we trained our model on 80% of our es data and tested it on 20%. This also means that we have predictions for only 20% of our data and thus the length of our predictions will not match the length of our es dataframe.

What we will have to do, given that we know from our classification report and confusion matrix that our model is valid, is fit our model to all of our es data so that we can get predictions for the other 80% of our data and be able to add them to our es dataframe.

We'll initialize a second predictions variable and pass in our entire X into our model.

#initializing second predictions variable for es dataframe predictions_2=model.predict(X.fillna(0))

Now we're ready to add our predictions to our es dataframe so that we can pass it into our rsi_strategy.

#adding our QDA model's predictions to our es dataframe es['Predictions']=predictions_2

Okay, we now have our predictions stored in our es dataframe. Now we can recalibrate our strategy so that if we have a prediction of "Down" or in other words if our model predicts a losing trade, we don't trade. Let's add this additional logic to our class.

class optimized_rsi(object):

def __init__(self,data,n,data_name,start,end):

self.data=data #the dataframe

self.n=n #the moving average

self.data_name=data_name #the name that will appear on plots

self.start=start #the beginning date of the sample period

self.end=end #the ending date of the sample period

def generate_signals(self):

delta=self.data[' Close'].diff()

dUp,dDown=delta.copy(),delta.copy()

dUp[dUp<0]=0 dDown[dDown>0]=0

RolUp=dUp.rolling(self.n).mean()

RolDown=dDown.rolling(self.n).mean()

#assigning indicator to the dataframe

self.data['RSI']=np.where(RolDown!=0, RolUp/RolDown,1)

self.data['RSI_Slow']=self.data['RSI'].rolling(self.n).mean()

#creating signals;

#altering the signal generator by going through our predictions

#and reinitializing signals to 0 whose prediction is down

self.data=self.data.assign(Signal=pd.Series(np.zeros(len(self.data))).values)

self.data['QDA Signal']=np.zeros(len(self.data))

self.data.loc[self.data['RSI']<self.data['RSI_Slow'],'Signal']=1 self.data.loc[self.data['RSI']>self.data['RSI_Slow'], 'Signal']=-1

self.data['QDA Signal']=np.where(self.data['Predictions']=="Down",0,self.data['Signal'])

return

def plot_performance(self,allocation):

#intializing a variable for initial allocation

#to be used to create equity curve

self.allocation=allocation

#creating returns and portfolio value series

self.data['Return']=np.log(self.data[' Close']/self.data[' Close'].shift(1))

#using our signal 2 column to calcuate returns instead of signal 1 column

self.data['S_Return']=self.data['QDA Signal'].shift(1)*self.data['Return']

self.data['Market_Return']=self.data['Return'].expanding().sum()

self.data['Strategy_Return']=self.data['S_Return'].expanding().sum()

self.data['Portfolio Value']=((self.data['Strategy_Return']+1)*self.allocation)

#creating metrics

self.data['Wins']=np.where(self.data['S_Return'] > 0,1,0)

self.data['Losses']=np.where(self.data['S_Return']<0,1,0)

self.data['Total Wins']=self.data['Wins'].sum()

self.data['Total Losses']=self.data['Losses'].sum()

self.data['Total Trades']=self.data['Total Wins'][0]+self.data['Total Losses'][0]

self.data['Hit Ratio']=round(self.data['Total Wins']/self.data['Total Losses'],2)

self.data['Win Pct']=round(self.data['Total Wins']/self.data['Total Trades'],2)

self.data['Loss Pct']=round(self.data['Total Losses']/self.data['Total Trades'],2)

#Plotting the Performance of the RSI Strategy

plt.plot(self.data['Market_Return'],color='black', label='Market Returns')

plt.plot(self.data['Strategy_Return'],color='blue', label= 'Strategy Returns')

plt.title('%s RSI Strategy Backtest'%(self.data_name))

plt.legend(loc=0)

plt.tight_layout()

plt.show()

plt.plot(self.data['Portfolio Value'])

plt.title('%s Portfolio Value'%(self.data_name))

plt.show()Now that we have altered our signal generator to account for our QDA model's predictions, let's initialize our strat2 object and compare our performance to that of our strat1 strategy.

#initializing our strat2 strategy strat2=optimized_rsi(es,10,'ES',es.iloc[0]['Date'],es.iloc[-1]['Date'])

#generating signals strat2.generate_signals()

Now that we have our signals based on our QDA model's predictions, we can call our plot_performance method to create our equity curve and then compare the metrics of our two strategy implementations.

#plotting performance strat2.plot_performance(10000)

Now that we have created the second instance of our momentum strategy we can calculate our metrics and compare the two our strat1 strategy.

#generating metrics strat2_trades=strat2.data['Total Trades'][0] strat2_hit_ratio=strat2.data['Hit Ratio'][0] strat2_win_pct=strat2.data['Win Pct'][0] strat2_loss_pct=strat2.data['Loss Pct'][0]

#printing strat2 metrics

print('Strat 2 Hit Ratio:',strat2_hit_ratio)

print('Strat 2 Win Percentage:',strat2_win_pct)

print('Strat 2 Loss Percentage:',strat2_loss_pct)

print('Strat 2 Total Trades:',strat2_trades)Strat 2 Hit Ratio: 0.97 Strat 2 Win Percentage: 0.49 Strat 2 Loss Percentage: 0.51 Strat 2 Total Trades: 1323

Let's store recall our strat1 metrics.

#getting strat1 metrics strat1_trades=strat1.data['Total Trades'][0] strat1_hit_ratio=strat1.data['Hit Ratio'][0] strat1_win_pct=strat1.data['Win Pct'][0] strat1_loss_pct=strat1.data['Loss Pct'][0]

#printing our strat1 metrics

print('Strat 1 Hit Ratio:',strat1_hit_ratio)

print('Strat 1 Win Percentage:',strat1_win_pct)

print('Strat 1 Loss Percentage:',strat1_loss_pct)

print('Strat 1 Total Trades:',strat1_trades)Strat 1 Hit Ratio: 0.93 Strat 1 Win Percentage: 0.48 Strat 1 Loss Percentage: 0.52 Strat 1 Total Trades: 22431

Okay, something interesting has happened. Recall earlier I stated that the fact that we only win 48% of the time wasn't the issue, the issue was shifting the probability in our favour, and limiting our losing trades. This is why we built our QDA model so that we could predict with a high degree of confidence when we were likely to take a trade that would result in a loss.

Notice that our metrics have changed slightly.

- Our strat2 Hit Ratio did improve somewhat and increase to .97 versus .93 for strat1.

- Our strat2 Win Pct increased to .49 from .48 in strat1 which also corresponds to a Loss Pct of .51 for strat2 and .52 for strat1.

Notice the significant difference in the number of trades that we took. We took substantially more trades in our strat1 instance versus that of our strat2 instance.

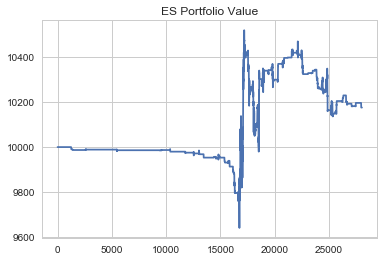

This directly affects the probability of our strategy making it to production. We effectively eliminated a lot of the trades that posed an issue for our strategy using our QDA model. Also, look at the equity curves of our strat1 and strat2 instances.

- Our strat1 instance finished the period down at a portfolio value of approximately 9600.

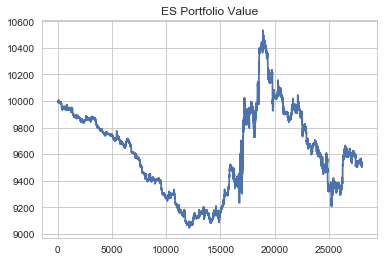

- Our strat2 instance finished the period up with a portfolio value of 10,200 which is less than its runup but still a significant improvement to that of the strat1 instance.

This is significant given the small change in our Win and Loss Percentages and shows that there are other factors present that play a major role in the profitability of a trading strategy. If you look closely at the end of the period, you can see the true effect of our QDA model. Toward the end of the period during our strat1 instance, we simply sold off in a straight line. But taking a look at our strat2 instance over the same time frame, we actually improved our trading significantly.

Naturally, relative to this strategy, there is a lot more that can be done to build upon what we've learned here. But, this experiment has proven that the framework presented here is a viable one for optimizing intraday trading strategies. Admittedly, the strategy presented in this post was designed to have flaws to test the idea of using QDA for optimization. In other words, I didn't attempt to optimize the strategy and merely wanted one that showed some potential much like strategies you may be working on currently. So imagine what you could do with this framework and a strategy you're actually trying to bring to production.

Review

We've covered a lot in this post and hopefully, you gained insight that can help you in strategy development.

We began by gaining an understanding of what QDA is and took a look at some of the math behind the model. We reviewed what learned in a prior post on LDA and made comparisons to that of QDA. We imported some intraday data on the eMini S&P 500 with the objective of creating an intraday momentum strategy and using QDA to improve our strategy. Before constructing our strategy we did some exploratory data analysis to learn more about our dataset.

We used object-oriented programming to design our RSI strategy in a way that would allow us to reuse our code and make multiple strategy instances. After creating our first strategy instance, we saw that our strategy was not production ready, but showed some signs of potential. Our objective was then to build a QDA model to predict when we might take a losing trade prior to us doing so in an effort to shift the probability of our strategy making it to production back in our favour.

We added a categorical column, Return Direction, to our data, and engineered features, Lag 3, 4, and 5 of volatility as well as our RSI to be used in our QDA model. Our QDA model showed a 92% Accuracy for being able to predict losing trades. We then applied our predictions to our data and created a strat2 instance. Though our Win and Loss Percentages changed marginally, our return increased by $600 and our strat2 instance, unlike our strat1 instance, actually finished the period positively.

Our research showed that our Intraday Machine Learning Optimization framework is viable for increasing the probability of bringing our strategies to production. There is a lot more than we can do to improve this strategy but the general idea has been conveyed.

Challenge: Send Us A Snapshot of Your Equity Curve On Twitter

Next Steps

Disclaimer: All investments and trading in the stock market involve risk. Any decisions to place trades in the financial markets, including trading in stock or options or other financial instruments is a personal decision that should only be made after thorough research, including a personal risk and financial assessment and the engagement of professional assistance to the extent you believe necessary. The trading strategies or related information mentioned in this article is for informational purposes only.

Download Data File

- Data CSV File