By Lamarcus Coleman

In this post, we will learn about the Stereoscopic Portfolio Optimization (SPO) framework and how it can be used to improve a quantitative trading strategy.

We'll also review concepts such as

- Gaussian Mixture Models,

- K-Means Clustering, and

- Random Forests.

Our objective is to determine whether we can reject the null hypothesis that the Stereoscopic Portfolio Optimization (SPO) model is not a viable option for creating optimal short-term portfolios.

This article covers:

- What is the Stereoscopic Portfolio Optimization (SPO) Framework?

- What are the Gaussian Mixture Models and how are they related to K-Means Clustering?

- Let's review Random Forests

- Portfolio Construction: Equal Weighted

- Portfolio Construction: Efficient Frontier

- Portfolio Construction: Bottom Up Optimization

- Portfolio Construction: SPO Framework

- Relative Portfolio Performance Assessment

- Summary

What is the Stereoscopic Portfolio Optimization (SPO) Framework?

The Stereoscopic Portfolio Optimization (SPO) Framework is an idea I introduced in a paper entitled "Applying Machine Learning Ensembles to Market Microstructure to Achieve Portfolio Optimization".

You can download the paper and files at the end of the article.

In the paper, I refer to traditional techniques such as the Efficient Frontier, as being top-down approaches to achieve an optimal portfolio.

Traditionally, a large part of portfolio optimization has centred on finding the proper balance for allocations to different asset classes based on the mean-variance tradeoff.

What the SPO Framework does

The Stereoscopic Portfolio Optimization Framework introduces the idea of bottom-up optimization via the use of machine learning ensembles applied to some market microstructure component.

In the text volatility was the microstructure component used but other components such as order arrival rates, liquidity, can be substituted into the framework.

Creating an SPO Framework

These bottom-up techniques are combined with top-down approaches to creating the Stereoscopic Portfolio Optimization (SPO) Framework.

Premise of the SPO Framework

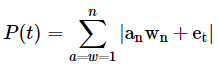

The premise of the framework is that a portfolio is the sum of n market microstructures.

The equation below was given as a novel way of explaining this logic.

This equation is a novel way of stating that the static state of a portfolio is a product of the component market microstructures and their weights.

Where,

'an' represents the nth asset's microstructure;

'wn' represents the weight of the nth asset;

'et' is an error term and representative of randomness.

The absolute value signs were used as an indication of non-linearity.

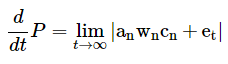

The equation below was offered as a novel representation of the dynamic state of a portfolio.

The equation above is stating that the dynamic state of the portfolio is not only dependent upon the respective components' microstructures but their relative correlations as well.

The correlations in this context don't refer to prices but the relationships between the actual microstructure components. For instance, how does one asset respond when shocks occur in another asset, or when liquidity changes, etc.

The idea of the correlations of microstructure components can be written as a conditional probability.

where,

an is the nth asset's microstructure, and

q represents the qth asset's microstructure.

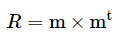

The correlation terms can thus be expressed in matrix form:

where,

R is the correlation matrix, and

m is a n×1 vector of our microstructure components

We can thus update our novel equation to the following:

Ensembles were used consistent with the idea that a portfolio is the composition of n market microstructures.

The strength of ensembles is that they allow for the aggregation of multiple, sometimes weak models, to create a more robust model.

- The goal of the ensemble is to minimize the cost function.

- The goal of portfolio optimization is to minimize risk.

Thus, in this context, the risk is the cost function of portfolio optimization and creates a parallel objective to that of ensembles.

In the paper, the Stereoscopic Portfolio Optimization (SPO) framework was created by combining the traditional mean-variance optimization with Gaussian Mixture Models and Random Forests. K-Means Clustering was used to identify subgroups within the S&P 500.

Before we dive into applying the Stereoscopic Portfolio Optimization (SPO) Framework to an intraday strategy, let's review some of the components used.

What are the Gaussian Mixture Models and how are they related to K-Means Clustering?

An important part of conducting research is understanding how your data is distributed. The distribution of your data gives you insight into the probabilities surrounding seeing certain observations.

In a prior post on K-Means Clustering, we learned what K-Means is and how it can be applied to statistical arbitrage. In short, unsupervised learning methods allow us to explore our data and identify patterns or relationships.

K-Means is a machine learning technique that seeks to identify subgroups within our data. This means that we can find relationships within our stock universe and then test to see if those relationships have some statistical significance.

For a more thorough review of K-Means, visit the series entitled "Using K-Means Clustering for Pair Selection".

Gaussian Mixture Models are similar to K-Means in that they too are a clustering technique. One key difference between GMM and K-Means is that K-Means is a hard clustering method while GMMs are referred to as being a soft clustering technique.

In K-Means an observation only has a probability of 0 or 1 of being in the kth class.

Gaussian Mixture Models don't assign a hard probability of being in a specific class but rather assigns a probability between 0 and 1 that observation came from a specific class.

Recall that in K-Means we begin by randomly assigning cluster centres placing each observation into a specific cluster.

We then compute the centroid or mean of the clusters. We then reassign points to each cluster based on their distance from the mean of each cluster.

This process is repeated until there are no more cluster reassignments. Our cost function in K-Means is to minimize the within-cluster variation or in laymen's terms ensure that the observations within each cluster are highly similar.

Below is the objective function for K-Means.

Where,

mk is the Mu of the kth cluster,

x(n) are our observations,

r(n)k is the probability of the nth observation belonging to the kth class.

Essentially in our K-Means objective function, we are multiplying the probabilities by the squared distances of each observation from the mean of the kth class.

Similar to K-Means, Gaussian Mixture Models begin by assigning random values for the parameters. It then calculates the probabilities of an observation coming from each of the kth distributions.

Unlike in K-Means in which we would set the probability to 1 or 0, Gaussian Mixture Models will calculate a probability of the observation coming from each of the k distributions.

Note that the sum of these probabilities must equal 1.

Below is an equation for the Gaussian Mixture Model:

Where,

πk is the probability of an observation belonging to the kth distribution;

N(μk,σk) represents a Gaussian distribution with a mean of μk and sigma of σk.

Note here that σk is a matrix composed of the product of the sum of the distances and the transpose of the distances multiplied by the probability that kth Gaussian generated the nth observation.

This is then averaged across the number of distributions.

Below is the equation for the σk term:

The gamma, γ, the term is the responsibility of the kth Gaussian for generating the nth point.

By responsibility, we are referring to the extent that the kth Gaussian contributed to the creation of the nth point.

We can compute the gamma, γ, term by the following equation.

The above equation is the quotient of the kth Gaussian and all of the Gaussians, or in other words the proportion of the kth Gaussian.

Let's Review Random Forests

Random Forests is a machine learning ensemble that combines several decision trees to make a single prediction. Recall that decision trees are known for their simplicity and ease of interpretation.

Bagging and boosting are alternatives to Random Forests that produce multiple trees. Trees can be applied to both regression and classification problems.

A decision tree divides the feature space into separate regions and every observation that falls into a specific region is given a prediction of the mean of that region.

The goal is to minimize the following cost function:

The above cost function is the Residual Sum of Squares and denotes the sum of the squared distances from the mean of the ith observation from the mean of the jth region, R.

Recursive binary splitting is conducted to minimize the RSS.

- The process considers every possible cutpoint, or point to split the space, of every feature with the aim of minimizing the cost function.

- This process is continued across the two new regions.

- These regions then undergo the same binary splitting as well.

- This is continued until a specific criterion is met.

One major consideration of decision trees is that if we grow a tree significantly large, it could overfit our data.

A smaller tree could lead to a better bias-variance tradeoff. A viable approach is to grow a large tree and then prune it, selecting only a subset of the tree. This is achieved via a process known as cost-complexity pruning.

Within cost-complexity pruning, we use a tuning parameter to select a sequence of subtrees.

Once we have a subset of trees we can then use k-fold cross-validation to choose the best value of the tuning parameter.

The tuning parameter a corresponds to a specific partition of the original tree. Thus when we perform k-fold cross-validation to find the value of a that achieves the best MSE, we can then select the corresponding subtree from our original tree.

Another key consideration of decision trees is that they can be non-robust. This means that a small change in the data can cause a large change in the tree. They can also lag in performance compared to other machine learning methods.

Random Forests is one method of improving the use of decision trees. Random Forests are similar to bagging decision trees in that they both resample the data and apply the model to the resamples and then average the results.

However, in Random Forests, when splitting is performed, a random sample of the features are selected as the split candidates. This is done to limit the influence of any one feature. So when splitting in Random Forests, we only consider m ∈ p possible features.

The reason Random Forests selects a fraction of the feature space at each split is that if there is a very strong feature in the space, it is likely to be chosen as the root node of every tree.

This would mean that each tree would likely be closely correlated and thus defeats the purpose of reducing variance.

Problem Statement

We need to construct a portfolio of statistical arbitrage strategies in the most efficient manner possible.

We will be trading on an intraday basis in the U.S. equities market, namely across stocks within the S&P 500.

We will design multiple portfolios that use various methods of addressing the portfolio optimization problem. To assess our efforts we will create the Sharpe Ratio of each portfolio and make relative comparisons.

Each portfolio will be composed of the same relationships to ensure apples to apple comparison.

Data

We will be using 5minute data over the period of 2018, beginning 1/4/18. Though at this point, we're unsure as to exactly which stocks we will be trading, we know that we will have the following four portfolios:

- Equally Weighted,

- Efficient Frontier,

- Bottom Up Optimization and

- Stereoscopic Portfolio Optimization (SPO) Framework.

The Equally Weighted Portfolio is the simplest to construct but because the remaining portfolios will require a training period, our test or assessment period will be the second half of 2018, indicating that our equally weighted portfolio will be constructed over the second half of our 2018 data.

This period will begin on May 1 and end June 12 2018. The remainder of our portfolios will be constructed using the first half of 2018 as a training period and the second half as the test or assessment period.

As we shall see, this is necessary to compare each portfolio over the same period. In short, in order to compose the Efficient Frontier, Bottom-Up, and SPO Portfolios, we first must have some period to train over (i.e. the first half of our 2018 data).

We need this training period so that we can make predictions over the period that we would like to compare all of the portfolios over (i.e. May 1 to June 12, 2018).

Our Equally Weighted Portfolio doesn't need a training period to be created so we will just create it over the period that will be used as the test period for the remaining portfolios.

Finding Tradeable Relationships

As we have covered in prior posts, a key initial problem to solve with developing a statistical arbitrage strategy is that of pair selection. We will once again use K-Means clustering to solve this problem.

We will apply K-Means to the S&P 500, create subgroups, and then choose five tradeable relationships to construct our portfolios.

To get started, let's import our usual libraries.

#data analysis and manipulation

import numpy as np

import pandas as pd

#data visualization

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')

#statistics and machine learning

from statsmodels.tsa.api import adfuller

from sklearn.cluster import KMeans

from sklearn.mixture import GaussianMixture as GM

from sklearn.ensemble import RandomForestClassifier as RF

from sklearn.metrics import confusion_matrix, classification_reportimport warnings

warnings.simplefilter('ignore')We're going to use the P/E, EPS, and Market Cap as our features to identify subgroups within the S&P 500.

Let's import our features data now.

#importing the Excel file that contains our features data

fundamentals=pd.ExcelFile('SPO_Data.xlsx')#parsing the Fundamentals sheet from our Excel file of which holds our P/E, EPS, and MarketCap data

features=fundamentals.parse('Fundamentals')Now that we have our features for our K-Means algorithm, let's check the head of our feature space.

#checking the head of our features dataframe features.head()

| No. | Symbol | Name | P/E | EPS | MarketCap |

|---|---|---|---|---|---|

| 0 | MMM | 3M Company | 23.17 | 8.16 | 112.74 |

| 1 | ABT | Abbott Laboratories | 48.03 | 0.94 | 77.76 |

| 2 | ABBV | AbbVie | 17.55 | 3.63 | 101.52 |

| 3 | ACN | Accenture plc | 18.37 | 6.76 | 77.29 |

| 4 | ATVI | Activision Blizzard | 37.55 | 1.28 | 36.13 |

We're now ready to create our K-Means method and find subgroups within the S&P 500.

Before we do so, let's drop the Name column from our features data.

#dropping name column

features.drop('Name',axis=1,inplace=True)#rechecking our data features.head()

| No. | Symbol | P/E | EPS | MarketCap |

|---|---|---|---|---|

| 0 | MMM | 23.17 | 8.16 | 112.74 |

| 1 | ABT | 48.03 | 0.94 | 77.76 |

| 2 | ABBV | 17.55 | 3.63 | 101.52 |

| 3 | ACN | 18.37 | 6.76 | 77.29 |

| 4 | ATVI | 37.55 | 1.28 | 36.13 |

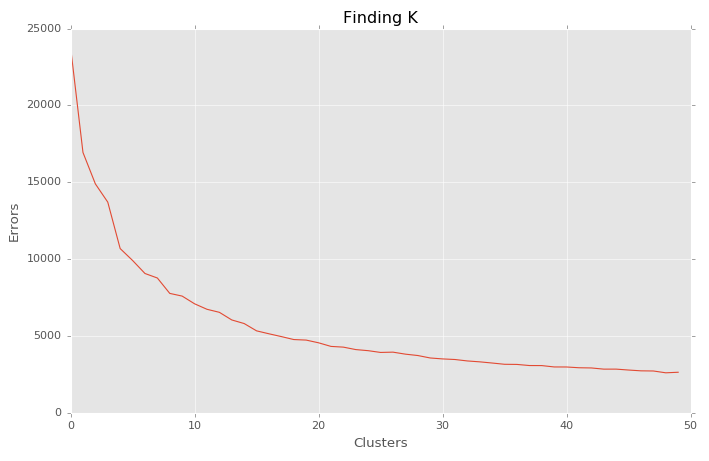

Recall, an early consideration for implementing K-Means Clustering is determining the value of K that should be used.

We'll use the elbow technique here to determine what value of K we should use. This technique will compare our value for K with the respective error.

Our goal is to choose the value for K that minimizes the error or cost function.

from scipy.spatial.distance import cdist

#creating our elbow technique method

def find_k(features):

#intializing a list to hold costs or errors

costs=[]

#iterating over possible values for k

for k in range(1,51):

model=KMeans(n_clusters=k)

model.fit(features)

costs.append(sum(np.min(cdist(features,model.cluster_centers_,'euclidean'),axis=1)))

#plotting our elbow graph

with plt.style.context(['classic','ggplot']):

plt.figure(figsize=(10,6))

plt.plot(costs)

plt.xlabel('Clusters')

plt.ylabel('Errors')

plt.title('Finding K')

plt.show()Now that we have our method let's use it to find the optimal value for K. First, let's update our dataframe by making using our Symbols as our index.

We'll first make a copy of our original dataframe.

#making a copy of our original features dataframe features_copy=features.copy()

Now we can reindex our features dataframe by our Symbol column.

#reindexing our features dataframe features_copy=features_copy.reindex(index=features_copy['Symbol'],columns=features_copy.columns)

features_copy.head()

| Symbol | Symbol | P/E | EPS | MarketCap |

|---|---|---|---|---|

| MMM | NaN | NaN | NaN | NaN |

| ABT | NaN | NaN | NaN | NaN |

| ABBV | NaN | NaN | NaN | NaN |

| ACN | NaN | NaN | NaN | NaN |

| ATVI | NaN | NaN | NaN | NaN |

Now that we have reindexed our features_copy dataframe, let's add back the values to our columns and drop the Symbol column.

#adding our data back to their respective columns features_copy['P/E']=features['P/E'].values features_copy['EPS']=features['EPS'].values features_copy['MarketCap']=features['MarketCap'].values

Okay. Let's recheck our dataframe.

features_copy.head()

| Symbol | Symbol | P/E | EPS | MarketCap |

|---|---|---|---|---|

| MMM | NaN | 23.17 | 8.16 | 112.74 |

| ABT | NaN | 48.03 | 0.94 | 77.76 |

| ABBV | NaN | 17.55 | 3.63 | 101.52 |

| ACN | NaN | 18.37 | 6.76 | 77.29 |

| ATVI | NaN | 37.55 | 1.28 | 36.13 |

Now we're ready to drop the Symbol column from our dataframe.

#dropping symbol column

features_copy.drop('Symbol',axis=1,inplace=True)Let's recheck our dataframe by calling the head method.

features_copy.head()

| Symbol | P/E | EPS | MarketCap |

|---|---|---|---|

| MMM | 23.17 | 8.16 | 112.74 |

| ABT | 48.03 | 0.94 | 77.76 |

| ABBV | 17.55 | 3.63 | 101.52 |

| ACN | 18.37 | 6.76 | 77.29 |

| ATVI | 37.55 | 1.28 | 36.13 |

Now let's use our find_k method to find the optimal value for K.

#finding K find_k(features_copy.fillna(0))

Okay, we will use 15 as our value for K. Now we're ready to implement our K-Means Clustering algorithm with K equal to 15 and look for tradable relationships.

Let's begin by initializing our model.

#initialzing K-Means algorithm kmeans=KMeans(n_clusters=15,random_state=101)

Notice that I used random_state=101. This is so that you can recreate the same results posted here. We will now fit our K-Means Algorithm to our features data.

#fitting kmeans to our features data kmeans.fit(features_copy.fillna(0))

KMeans(algorithm='auto', copy_x=True, init='k-means++', max_iter=300,

n_clusters=15, n_init=10, n_jobs=1, precompute_distances='auto',

random_state=101, tol=0.0001, verbose=0)Note that we called the fillna method on our features_copy dataframe and replaced NaNs values with 0. We can now review our clusters.

Let's start by checking our labels.

#getting cluster labels kmeans.labels_

array([ 6, 6, 6, 6, 12, 3, 0, 3, 13, 0, 3, 3, 12, 12, 12, 3, 3,

7, 3, 6, 12, 3, 3, 1, 1, 5, 14, 3, 3, 12, 6, 0, 12, 3,

3, 3, 3, 6, 3, 13, 3, 0, 3, 13, 3, 8, 0, 3, 13, 3, 3,

2, 13, 0, 13, 3, 3, 3, 13, 12, 2, 12, 13, 0, 0, 13, 13, 3,

0, 0, 3, 6, 7, 12, 7, 6, 6, 13, 3, 3, 13, 12, 0, 3, 3,

0, 0, 12, 3, 3, 6, 3, 3, 3, 3, 13, 0, 6, 13, 5, 10, 0,

3, 0, 13, 3, 3, 5, 5, 3, 3, 0, 3, 3, 5, 0, 0, 5, 3,

3, 13, 0, 3, 3, 3, 6, 13, 7, 3, 0, 3, 6, 3, 0, 3, 3,

0, 3, 0, 12, 13, 12, 3, 3, 3, 3, 3, 0, 3, 6, 3, 3, 0,

0, 12, 3, 3, 0, 0, 0, 3, 12, 3, 0, 13, 13, 0, 13, 12, 11,

13, 12, 3, 3, 0, 7, 3, 0, 3, 9, 3, 9, 3, 12, 0, 12, 3,

13, 13, 3, 3, 12, 3, 12, 3, 3, 0, 3, 3, 3, 13, 13, 3, 3,

0, 2, 3, 0, 0, 3, 6, 12, 6, 13, 3, 0, 3, 3, 3, 3, 3,

3, 0, 3, 13, 3, 13, 0, 12, 5, 6, 3, 3, 3, 12, 3, 12, 0,

12, 11, 3, 5, 3, 5, 3, 3, 3, 12, 12, 3, 7, 3, 3, 3, 9,

0, 9, 3, 3, 12, 3, 0, 3, 7, 3, 3, 6, 3, 3, 3, 3, 3,

3, 3, 7, 3, 6, 3, 12, 3, 6, 3, 6, 0, 3, 3, 3, 3, 13,

3, 12, 0, 12, 3, 6, 3, 3, 6, 0, 3, 6, 5, 7, 12, 13, 11,

13, 1, 12, 3, 3, 0, 0, 12, 7, 6, 3, 13, 12, 7, 13, 13, 12,

4, 12, 13, 13, 13, 13, 0, 12, 6, 3, 13, 3, 0, 3, 0, 13, 3,

0, 3, 0, 3, 12, 5, 12, 3, 3, 3, 0, 3, 3, 5, 3, 13, 5,

0, 5, 0, 3, 13, 0, 12, 12, 3, 0, 6, 3, 2, 3, 3, 0, 3,

0, 3, 3, 13, 6, 3, 3, 13, 0, 12, 12, 12, 12, 3, 12, 6, 3,

3, 3, 12, 3, 3, 3, 0, 4, 3, 6, 3, 3, 3, 3, 3, 13, 0,

3, 12, 3, 0, 0, 13, 3, 13, 6, 3, 12, 0, 3, 13, 3, 3, 3,

3, 3, 3, 12, 3, 6, 3, 0, 3, 12, 12, 12, 0, 5, 0, 3, 6,

0, 3, 12, 3, 3, 13, 12, 0, 0, 3, 6, 12, 12, 12, 12, 6, 3,

5, 6, 3, 6, 3, 3, 3, 3, 3, 3, 12, 3, 3, 5, 13, 3, 5,

3, 12, 5, 6, 0, 3, 3, 2, 3, 13, 12, 7, 3, 3, 3, 13, 12,

3, 12, 3, 13, 3, 3, 12, 0, 3, 7, 3, 12])We will now add our cluster assignments back to our dataframe.

#adding cluster labels to dataframe features_copy['Cluster']=kmeans.labels_

Let's now review our features dataframe

#reviewing features dataframe features_copy.head()

| Symbol | P/E | EPS | MarketCap | Cluster |

|---|---|---|---|---|

| MMM | 23.17 | 8.16 | 112.74 | 6 |

| ABT | 48.03 | 0.94 | 77.76 | 6 |

| ABBV | 17.55 | 3.63 | 101.52 | 6 |

| ACN | 18.37 | 6.76 | 77.29 | 6 |

| ATVI | 37.55 | 1.28 | 36.13 | 12 |

#calling tail method our dataframe features_copy.tail()

| Symbol | P/E | EPS | MarketCap | Cluster |

|---|---|---|---|---|

| YHOO | NaN | -0.23 | 43.74 | 0 |

| YUM | 15.83 | 4.04 | 22.65 | 3 |

| ZBH | 77.53 | 1.51 | 23.54 | 7 |

| ZION | 22.75 | 1.99 | 9.17 | 3 |

| ZTS | 32.16 | 1.65 | 26.11 | 12 |

Now that we have our cluster assignments, let's group our data by the cluster assignments.

#creating dataframe to hold data clusters_df=pd.DataFrame() #grouping our data by cluster for clusters with atleast 2 stocks in it. clusters_df=pd.concat(i for clusters_df, i in features_copy.groupby(features_copy['Cluster']) if len(i) >1)

Let's now check of our new dataframe.

#checking the head of clusters df clusters_df.head()

| Symbol | P/E | EPS | MarketCap | Cluster |

|---|---|---|---|---|

| ADBE | 51.72 | 2.32 | 59.28 | 0 |

| AET | 20.37 | 6.41 | 45.93 | 0 |

| AIG | NaN | -0.78 | 62.15 | 0 |

| ANTM | 18.02 | 9.21 | 43.89 | 0 |

| AMAT | 19.02 | 1.94 | 39.92 | 0 |

#checking the tail of our cluster df clusters_df.tail()

| Symbol | P/E | EPS | MarketCap | Cluster |

|---|---|---|---|---|

| RIG | 6.09 | 2.10 | 4.67 | 13 |

| VRTX | NaN | -0.46 | 22.69 | 13 |

| WDC | NaN | -1.59 | 22.12 | 13 |

| WMB | NaN | -0.57 | 24.30 | 13 |

| XRX | NaN | -0.49 | 7.48 | 13 |

Now that we have our data organized by cluster assignment, we're ready to check for tradeable relationships.

To do this, we will create every possible pair combination within a respective cluster. We can then later run the CADF test on specific pairs from our clusters.

Let's create a method that will take the symbols from a specific cluster as an input, compute the possible pair combinations of a respective cluster and store our pairs into a separate list.

#creating method to identify each possible pair def create_pairs(symbolList): #creating a list to hold each possible pair pairs=[] #initializing placeholders for the symbols in each pair x=0 y=0 for count,symbol in enumerate(symbolList): for nextCount,nextSymbol in enumerate(symbolList): x=symbol y=nextSymbol if x !=y: pairs.append([x,y]) return pairs

We will now create a list of symbols. Let's use the stock symbols from cluster 0.

#creating list of symbols from cluster 0 symbol_list_0=['ADBE','AET','AIG','ANTM','AMAT']

We will now use our create pairs method above to create a list of lists of the possible pair combinations.

#list of lists of pairs all_pairs=create_pairs(symbol_list_0)

Let's check our pair combinations.

#printing list of all_pairs from cluster 0 all_pairs

[['ADBE', 'AET'], ['ADBE', 'AIG'], ['ADBE', 'ANTM'], ['ADBE', 'AMAT'], ['AET', 'ADBE'], ['AET', 'AIG'], ['AET', 'ANTM'], ['AET', 'AMAT'], ['AIG', 'ADBE'], ['AIG', 'AET'], ['AIG', 'ANTM'], ['AIG', 'AMAT'], ['ANTM', 'ADBE'], ['ANTM', 'AET'], ['ANTM', 'AIG'], ['ANTM', 'AMAT'], ['AMAT', 'ADBE'], ['AMAT', 'AET'], ['AMAT', 'AIG'], ['AMAT', 'ANTM']]

Okay. Now that we have our possible pair combinations from cluster 0, let's import our intraday data for these stocks.

#initializing our stock variables

adbe=pd.read_csv('ADBE_5min.csv')

aet=pd.read_csv('AET_5min.csv')

aig=pd.read_csv('AIG_5min.csv')

antm=pd.read_csv('ANTM_5min.csv')

amat=pd.read_csv('AMAT_5min.csv')Let's check our data.

#checking head of ADBE adbe.head()

| Date | Time | Open | High | Low | Close | Volume | NumberOfTrades | BidVolume | AskVolume | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2018/01/04 | 08:30:00 | 181.93 | 183.74 | 181.84 | 183.13 | 83862 | 396 | 22941 | 60921 |

| 1 | 2018/01/04 | 08:35:00 | 183.05 | 183.48 | 182.66 | 182.89 | 31593 | 238 | 17840 | 13753 |

| 2 | 2018/01/04 | 08:40:00 | 182.84 | 183.35 | 182.70 | 183.22 | 49654 | 345 | 26962 | 22692 |

| 3 | 2018/01/04 | 08:45:00 | 183.25 | 183.73 | 183.06 | 183.73 | 51108 | 314 | 21566 | 29542 |

| 4 | 2018/01/04 | 08:50:00 | 183.66 | 184.00 | 183.56 | 183.90 | 27476 | 196 | 15287 | 12189 |

#checking tail of AIG aig.tail()

| Date | Time | Open | High | Low | Close | Volume | NumberOfTrades | BidVolume | AskVolume | |

|---|---|---|---|---|---|---|---|---|---|---|

| 8574 | 2018/06/12 | 14:30:00 | 54.54 | 54.56 | 54.51 | 54.55 | 60902 | 357 | 20106 | 40796 |

| 8575 | 2018/06/12 | 14:35:00 | 54.55 | 54.61 | 54.53 | 54.60 | 74483 | 425 | 29354 | 45129 |

| 8576 | 2018/06/12 | 14:40:00 | 54.60 | 54.60 | 54.55 | 54.58 | 67539 | 414 | 20687 | 46852 |

| 8577 | 2018/06/12 | 14:45:00 | 54.57 | 54.58 | 54.54 | 54.56 | 82122 | 439 | 24925 | 57197 |

| 8578 | 2018/06/12 | 14:50:00 | 54.56 | 54.62 | 54.56 | 54.60 | 120328 | 779 | 46340 | 73988 |

We can see that we have 5 min bar data for our stocks ranging from January 3, 2018, to the first half of the session on June 11, 2018.

We can now test our pairs for cointegration. Recall that we are going to use part of our data as our assessment period so we don't want to include it in our test.

We'll use January to May as our training period and assess our portfolios over the remainder of our data. Let's create variables to hold our training period data.

We'll store use our Close column. So that we can parse out our data by our training period, we'll make our date column the index of our data.

We begin by making a copy of our data. Let's create a method to perform this across our symbols data.

We'll store our original symbols data in a dictionary and pass it into our function.

#creating list to hold original data

original_data={'ADBE':adbe,'AET':aet,'AIG':aig,'ANTM':antm,'AMAT':amat}We can now create our function to copy our original data and create a dataframe for our training period data.

#function to parse out training period data

def get_training_data(original_data,symbol_list,start,end):

'''

PARAMETERS:

original_data - the dictionary we created that holds our dataframes

symbol_list - the list of symbols; data type are strings

start - the beginning date of our training period as a string

end - the ending date of our training period as a string

'''

#creating a dataframe to hold our parsed series

training_df=pd.DataFrame()

#iterating over our symbol list

for count, symbol in enumerate(symbol_list):

try:

#making a copy of our original data for each symbol

copy=original_data[symbol].copy()

#reindexing our copied data by Date column

copy=copy.reindex(index=copy['Date'],columns=copy.columns)

#restoring values of close column from our original data

copy[' Close']=original_data[symbol][' Close'].values

#parsing out our training period

copy=copy.loc[start:end][' Close']

#adding training data to dataframe

training_df[str(symbol)]=copy.values

except:

print(str(symbol),'Threw an Exception')

print('Current Symbol Length:')

print(len(copy.loc[start:end]))

print("")

print('training_df Length:')

print(len(training_df))

continue

return training_df

We're now ready to create our training data.

We'll use our get_training_data function to parse out our training data and then use this dataframe to parse out the respective series for our pair combinations to perform our CADF test.

#creating our training data dataframe using our training period start and end dates training_df=get_training_data(original_data,symbol_list_0,'2018/01/04','2018/04/30')

Let's check our training_df.

training_df.head()

| ADBE | AET | AIG | ANTM | AMAT | |

|---|---|---|---|---|---|

| 0 | 183.13 | 183.45 | 60.36 | 229.62 | 54.67 |

| 1 | 182.89 | 183.68 | 60.61 | 229.63 | 54.51 |

| 2 | 183.22 | 183.80 | 60.77 | 229.70 | 54.25 |

| 3 | 183.73 | 183.82 | 60.81 | 229.65 | 54.08 |

| 4 | 183.90 | 183.93 | 60.80 | 229.70 | 54.27 |

After checking our dataframe, we find that we have our training period data for all of our stocks. This means that we should have 20 possible pairs.

We can write a method to check our math.

#creating method to check possible pair combinations def possitrainingnations(n): #Parameters# ############ #n- represents the number of items or in our case stocks possible_pairs=(n*(n-1)) return possible_pairs

Now let's check our possible pair combinations.

#checking possible pair combinations possible_combinations(5) # we pass in 5 for our 5 stocks

20

We're now ready to check our pairs for cointegration.

We'll create a method that will allow us to iterate over our pairs, compute the slope and then perform the CADF test. The pairs that are cointegrated will be stored in a list.

Let's import our OLS method.

from scipy.stats import linregress

Now we'll write our method to create our cointegrated pairs.

def get_cointegrated(all_pairs,training_df):

'''

PARAMETERS

#########

all_pairs - the list of all possible pair combinations from Cluster 0

training_df - our dataframe holding our stock data for stocks in Cluster 0 over the training period

'''

#creating a list to hold cointegrated pairs

cointegrated=[]

#iterate over each pair in possible pairs list; pair is a list of our 2 stock symbols

for count, pair in enumerate(all_pairs):

try:

#getting data for each stock in pair from training_df

ols=linregress(training_df[str(pair[1])],training_df[str(pair[0])]) #note scipy's linregress takes in Y then X

#storing slope or hedge ratio in variable

slope=ols[0]

#creating spread

spread=training_df[str(pair[1])]-(slope*training_df[str(pair[0])])

#testing spread for cointegration

cadf=adfuller(spread,1)

#checking to see if spread is cointegrated, if so then store pair in cointegrated list

if cadf[0] < cadf[4]['1%']:

print('Pair Cointegrated at 99% Confidence Interval')

#appending the X and Y of pair

cointegrated.append([pair[0],pair[1]])

elif cadf[0] < cadf[4]['5%']:

print('Pair Cointegrated at 95% Confidence Interval')

#appending the X and Y of pair

cointegrated.append([pair[0],pair[1]])

elif cadf[0] < cadf[4]['10%']:

print('Pair Cointegrated at 90% Confidence Interval')

cointegrated.append(pair[0],pair[1])

else:

print('Pair Not Cointegrated ')

continue

except:

print('Exception: Symbol not in Dataframe')

continue

return cointegrated

Let's initialize our get_cointegrated function and find our cointegrated pairs.

#getting our cointegrated pairs cointegrated_from_cluster_0=get_cointegrated(all_pairs,training_df)

Pair Not Cointegrated Pair Not Cointegrated Pair Cointegrated at 95% Confidence Interval Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Cointegrated at 95% Confidence Interval Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Cointegrated at 95% Confidence Interval Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated Pair Not Cointegrated

Let's check our cointegrated list.

cointegrated_from_cluster_0

[['ADBE', 'ANTM'], ['AET', 'ANTM'], ['ANTM', 'AET']]

Okay. We've found that 3 of our possible 20 pairs are cointegrated each at the 90% confidence interval.

Recall that we called the head method on our clusters_df dataframe of which returns only the first five rows.

Let's use the Counter method to get an idea of how our symbols are distributed across all our clusters.

#importing the Counter method from collections import Counter

#calling Counter method on our clusters Counter(clusters_df['Cluster'])

Counter({0: 76,

1: 3,

2: 5,

3: 215,

4: 2,

5: 19,

6: 39,

7: 13,

9: 4,

11: 3,

12: 69,

13: 54})We can see that Cluster 0 actually contains a total of 76 symbols. Given that we found 3 tradeable relationships, we'll use these.

However, I will illustrate how, in the event that none of the symbols in our first cluster were cointegrated, we would go about checking the symbols in a specific cluster.

We'll need to create a method that will allow us to iterate over our clusters column and return the symbols that are within a specific cluster.

To begin we'll add our symbols back to our dataframe as a column so that we can retrieve them if our cluster condition is met.

#adding Symbol Column back to cluster_df clusters_df['Symbol']=clusters_df.index

Let's recheck our dataframe.

#checking update to cluster_df clusters_df.head()

| Symbol | P/E | EPS | MarketCap | Cluster | Symbol |

|---|---|---|---|---|---|

| ADBE | 51.72 | 2.32 | 59.28 | 0 | ADBE |

| AET | 20.37 | 6.41 | 45.93 | 0 | AET |

| AIG | NaN | -0.78 | 62.15 | 0 | AIG |

| ANTM | 18.02 | 9.21 | 43.89 | 0 | ANTM |

| AMAT | 19.02 | 1.94 | 39.92 | 0 | AMAT |

Now we're ready to create our method of retrieving and storing our symbols in a list based on our cluster.

For this task, we'll use a list comprehension. We'll apply our method to cluster 9.

symbols_cluster_9=[ clusters_df['Symbol'][count] for count,value in enumerate(clusters_df['Cluster'].values) if value == 9]

Let's check the length of our symbols_cluster_9 list to ensure that our method worked correctly.

Recall that our Counter method returned a value of 4 for the number of symbols in this cluster.

#getting the length of our cluster 9 list len(symbols_cluster_9)

4

Great! We see that our list comprehension is working properly. Now we can use this list of symbols to create every possible pair combination for cluster 9.

Let's check what symbols are in cluster 9.

#checking the symbols in cluster 9 symbols_cluster_9

['XOM', 'FB', 'JNJ', 'JPM']

We'll now use this list to create our pair combinations for cluster 9 using our create_pairs method from earlier.

#getting pair combinations for cluster 9 cluster_9_pairs=create_pairs(symbols_cluster_9)

Let's check our pair combinations for cluster 9.

#checking cluster 9 pair combinations. cluster_9_pairs

[['XOM', 'FB'], ['XOM', 'JNJ'], ['XOM', 'JPM'], ['FB', 'XOM'], ['FB', 'JNJ'], ['FB', 'JPM'], ['JNJ', 'XOM'], ['JNJ', 'FB'], ['JNJ', 'JPM'], ['JPM', 'XOM'], ['JPM', 'FB'], ['JPM', 'JNJ']]

Okay. We've learned that we have three tradeable relationships from Cluster 0 from the first five symbols we tested. We've also walked through how we would find other pairs in other clusters if we had not found these three pairs.

After finding the pairs above, we would apply the same method to check for cointegration as was used to identify our three pairs.

From here we are ready to begin constructing our portfolios.

Brief Recap

Let's take a step back and review what we've accomplished thus far.

- We began by gaining an understanding of the Stereoscopic Portfolio Optimization (SPO) Framework.

- We then performed K-Means Clustering on the S&P 500.

- We found optimal value for K by creating the elbow graph using our fundamental data features.

- After finding K, we created our K-Means algorithm and selected stocks from Cluster 0 to test whether or not we could identify tradeable relationships.

Out of the first five symbols in Cluster 0, we found that 3 of the 20 possible combinations were cointegrated.

To illustrate how we would proceed had we not found any tradeable relationships, we created a method that would allow us to select all of the stocks from within a specific cluster and use these to create all possible pair combinations.

With these pairs in hand, we could then test these pairs to see if we could find tradeable relationships.

Portfolio Construction: Equal Weighted

Now that we have found some likely tradeable relationships, we're ready to construct our portfolio. In this section, we're going to create a portfolio that equally weighs our strategy.

We'll assume that we have a portfolio value of $100k USD with 10% in cash. We will allocate $30k USD to each of our pairs. To begin we will create a class that will allow us to create our StatArb strategies.

Recall, our training period for our portfolios that will be employing the use of machine learning is 1/4/2018 to 4/30/2018, thus because this portfolio will not be employing the use of an optimization method, we will construct it over the period beginning 5/1/2018 so that it is consistent with the test period of our remaining portfolios.

Let's now create the variables of each of our symbols that will hold the data beginning 5/1/2018.

We'll make a copy of our data and set our date as the index so that we can parse out our test period.

#creating copies of our data adbe_copy=adbe.copy() aet_copy=aet.copy() antm_copy=antm.copy()

#reindexing our data adbe_copy=adbe_copy.reindex(index=adbe_copy['Date'],columns=adbe_copy.columns) aet_copy=aet_copy.reindex(index=aet_copy['Date'],columns=aet_copy.columns) antm_copy=antm_copy.reindex(index=antm_copy['Date'],columns=antm_copy.columns)

Okay. Let's check our dataframe.

#checking dataframe after reindexing adbe_copy.head()

| Date | Date | Time | Open | High | Low | Close | Volume | NumberOfTrades | BidVolume | AskVolume |

|---|---|---|---|---|---|---|---|---|---|---|

| 2018/01/04 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2018/01/04 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2018/01/04 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2018/01/04 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2018/01/04 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

Now let's restore the values back to our columns. We'll also drop the date column.

#dropping date columns

adbe_copy.drop('Date',axis=1,inplace=True)

aet_copy.drop('Date',axis=1,inplace=True)

antm_copy.drop('Date',axis=1,inplace=True)#restoring our column values back to our data adbe_copy[[' Time',' Open',' High',' Low',' Close',' Volume',' NumberOfTrades',' BidVolume',' AskVolume']]=adbe[[' Time',' Open',' High',' Low',' Close',' Volume',' NumberOfTrades',' BidVolume',' AskVolume']].values aet_copy[[' Time',' Open',' High',' Low',' Close',' Volume',' NumberOfTrades',' BidVolume',' AskVolume']]=aet[[' Time',' Open',' High',' Low',' Close',' Volume',' NumberOfTrades',' BidVolume',' AskVolume']].values antm_copy[[' Time',' Open',' High',' Low',' Close',' Volume',' NumberOfTrades',' BidVolume',' AskVolume']]=antm[[' Time',' Open',' High',' Low',' Close',' Volume',' NumberOfTrades',' BidVolume',' AskVolume']].values

Let's recheck our dataframe.

#rechecking our dataframe adbe_copy.head()

| Date | Time | Open | High | Low | Close | Volume | NumberOfTrades | BidVolume | AskVolume |

|---|---|---|---|---|---|---|---|---|---|

| 2018/01/04 | 08:30:00 | 181.93 | 183.74 | 181.84 | 183.13 | 83862 | 396 | 22941 | 60921 |

| 2018/01/04 | 08:35:00 | 183.05 | 183.48 | 182.66 | 182.89 | 31593 | 238 | 17840 | 13753 |

| 2018/01/04 | 08:40:00 | 182.84 | 183.35 | 182.70 | 183.22 | 49654 | 345 | 26962 | 22692 |

| 2018/01/04 | 08:45:00 | 183.25 | 183.73 | 183.06 | 183.73 | 51108 | 314 | 21566 | 29542 |

| 2018/01/04 | 08:50:00 | 183.66 | 184.00 | 183.56 | 183.90 | 27476 | 196 | 15287 | 12189 |

Now we're ready to slice out our test period.

#creating variables to hold testing period data adbe_test=adbe_copy.loc['2018/05/01':] aet_test=aet_copy.loc['2018/05/01':] antm_test=antm_copy.loc['2018/05/01':]

Let's check the head and tail of our data.

#checking beginning of test period adbe_test.head()

| Date | Time | Open | High | Low | Close | Volume | NumberOfTrades | BidVolume | AskVolume |

|---|---|---|---|---|---|---|---|---|---|

| 2018/05/01 | 08:30:00 | 220.77 | 221.28 | 220.33 | 220.88 | 52351 | 233 | 39904 | 12447 |

| 2018/05/01 | 08:35:00 | 220.95 | 221.34 | 219.78 | 220.09 | 31969 | 242 | 15350 | 16619 |

| 2018/05/01 | 08:40:00 | 220.10 | 220.15 | 219.38 | 219.64 | 26163 | 175 | 14622 | 11541 |

| 2018/05/01 | 08:45:00 | 219.52 | 220.55 | 219.52 | 220.34 | 22756 | 117 | 10890 | 11866 |

| 2018/05/01 | 08:50:00 | 220.31 | 220.82 | 220.24 | 220.51 | 23994 | 89 | 18044 | 5950 |

#checking the end of test period adbe_test.tail()

| Date | Time | Open | High | Low | Close | Volume | NumberOfTrades | BidVolume | AskVolume |

|---|---|---|---|---|---|---|---|---|---|

| 2018/06/12 | 14:30:00 | 252.26 | 252.35 | 252.25 | 252.34 | 35644 | 285 | 15996 | 19648 |

| 2018/06/12 | 14:35:00 | 252.35 | 252.35 | 252.05 | 252.27 | 32074 | 261 | 14746 | 17328 |

| 2018/06/12 | 14:40:00 | 252.27 | 252.32 | 252.12 | 252.20 | 25809 | 222 | 13909 | 11900 |

| 2018/06/12 | 14:45:00 | 252.19 | 252.36 | 252.06 | 252.36 | 43128 | 340 | 19684 | 23444 |

| 2018/06/12 | 14:50:00 | 252.40 | 252.53 | 252.29 | 252.47 | 53480 | 450 | 25475 | 28005 |

We can now parse out our closing values from our test period dataframes.

#Closing price series for data adbe_test_price_series=np.array(adbe_test[' Close']) aet_test_price_series=np.array(aet_test[' Close']) antm_test_price_series=np.array(antm_test[' Close'])

Let's check one of our price series. We'll use AET.

#checking head of AET price series aet_test_price_series[0:5]

array([ 180.42, 179.7 , 179.3 , 179.53, 179.7 ])

We can now construct our StatArb class and create our individual strategies. We will then combine these individual strategies into an equally weighted portfolio.

class statarb(object):

def __init__(self,df1, df2,ma,floor, ceiling,beta_lookback,start,end,exit_zscore=0):

#setting the attributes

self.df1=df1 #array of prices for X

self.df2=df2 #array of prices for Y

self.ma=ma# the lookback period

self.floor=floor #the buy threshold for the z-score

self.ceiling=ceiling #the sell threshold for the z-score

self.Close='Close Long' #used as close signal for longs

self.Cover='Cover Short' #used as close signal for shorts

self.exit_zscore=exit_zscore #the z-score

self.beta_lookback=beta_lookback #the lookback for hedge ratio

self.start=start #the beginning of test period as a string

self.end=end # the end of test period as a string

#create price spread

def create_spread(self):

#creating new dataframe

self.df=pd.DataFrame(index=range(0,len(self.df1)))

try:

self.df['X']=self.df1

self.df['Y']=self.df2

except:

print('Length of self.df:')

print(len(self.df))

print('')

print('Length of self.df1:')

print(len(self.df1))

print('')

print('Length of self.df2:')

print(len(self.df2))

#calculating the beta of the pairs

ols=linregress(self.df['Y'],self.df['X'])

self.df['Beta']=ols[0]

#calculating the spread

self.df['Spread']=self.df['Y']-(self.df['Beta'].rolling(window=self.beta_lookback).mean()*self.df['X'])

return self.df.head()

def generate_signals(self):

#creating the z-score

self.df['Z-Score']=(self.df['Spread']-self.df['Spread'].rolling(window=self.ma).mean())/self.df['Spread'].rolling(window=self.ma).std()

#prior z-score

self.df['Prior Z-Score']=self.df['Z-Score'].shift(1)

#Creating Buy and Sell Signals; when to be long, short, exit

self.df['Longs']=(self.df['Z-Score']<=self.floor)*1.0 #buy the spread

self.df['Shorts']=(self.df['Z-Score']>=self.ceiling)*1.0 #short the spread

self.df['Longs_Exit']=(self.df['Z-Score']>=self.exit_zscore)*1.0

self.df['Shorts_Exit']=(self.df['Z-Score']<=self.exit_zscore)*1.0

#tracking positions via for loop implementation

self.df['Long_Market']=0.0

self.df['Short_Market']=0.0

#Setting Variables to track whether or not to be long while iterating over df

self.long_market=0

self.short_market=0

#Determining when to trade

for i,value in enumerate(self.df.iterrows()):

#Calculate longs

if value[1]['Longs']==1.0:

self.long_market=1

elif value[1]['Longs_Exit']==1.0:

self.long_market=0

elif value[1]['Shorts']==1.0:

self.short_market=1

elif value[1]['Shorts_Exit']==1.0:

self.short_market=0

self.df.iloc[i]['Long_Market']=self.long_market

self.df.iloc[i]['Short_Market']=self.short_market

return

def create_returns(self, allocation,pair_number):

'''

PARAMETERS

##########

allocation - the amount of capital alotted for pair

pair_number - string to annotate the plots

'''

self.allocation=allocation

self.pair=pair_number

self.portfolio=pd.DataFrame(index=self.df.index)

self.portfolio['Positions']=self.df['Long_Market']-self.df['Short_Market']

self.portfolio['X']=-1.0*self.df['X']*self.portfolio['Positions']

self.portfolio['Y']=self.df['Y']*self.portfolio['Positions']

self.portfolio['Total']=self.portfolio['X']+self.portfolio['Y']

#creating a percentage return stream

self.portfolio['Returns']=self.portfolio['Total'].pct_change()

self.portfolio['Returns'].fillna(0.0,inplace=True)

self.portfolio['Returns'].replace([np.inf,-np.inf],0.0,inplace=True)

self.portfolio['Returns'].replace(-1.0,0.0,inplace=True)

#calculating metrics

self.mu=(self.portfolio['Returns'].mean())

self.sigma=(self.portfolio['Returns'].std())

self.portfolio['Win']=np.where(self.portfolio['Returns']>0,1,0)

self.portfolio['Loss']=np.where(self.portfolio['Returns']<0,1,0)

self.wins=self.portfolio['Win'].sum()

self.losses=self.portfolio['Loss'].sum()

self.total_trades=self.wins+self.losses

#calculating sharpe ratio with interest rate of

#interest_rate_assumption=0.75

#self.sharp=(self.mu-interest_rate_assumption)/self.sigma

#win loss ratio;

self.win_loss_ratio=(self.wins/self.losses)

#probability of win

self.prob_of_win=(self.wins/self.total_trades)

#probability of loss

self.prob_of_loss=(self.losses/self.total_trades)

#average return of wins

self.avg_win_return=(self.portfolio['Returns']>0).mean()

#average returns of losses

self.avg_loss_return=(self.portfolio['Returns']<0).mean()

#calculating payout ratio

self.payout_ratio=(self.avg_win_return/self.avg_loss_return)

#calculate equity curve

self.portfolio['Returns']=(self.portfolio['Returns']+1.0).cumprod()

self.portfolio['Trade Returns']=(self.portfolio['Total'].pct_change()) #non cumulative Returns

self.portfolio['Portfolio Value']=(self.allocation*self.portfolio['Returns'])

self.portfolio['Portfolio Returns']=self.portfolio['Portfolio Value'].pct_change()

self.portfolio['Initial Value']=self.allocation

with plt.style.context(['ggplot','seaborn-paper']):

#Plotting Portfolio Value

plt.plot(self.portfolio['Portfolio Value'])

plt.plot(self.portfolio['Initial Value'])

plt.title('%s Strategy Returns '%(self.pair))

plt.legend(loc=0)

plt.show()

return

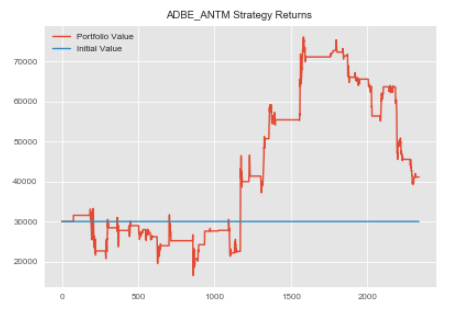

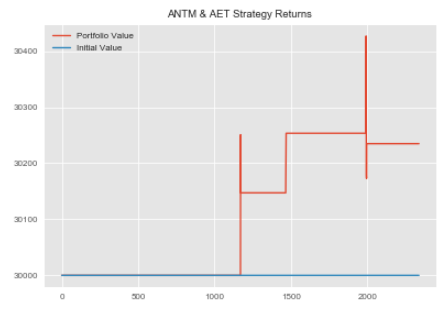

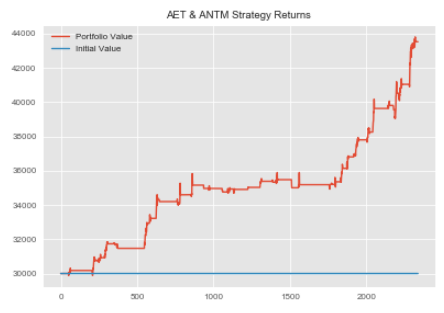

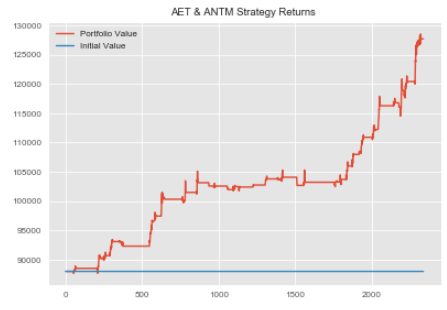

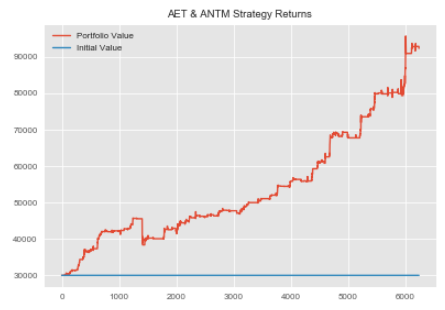

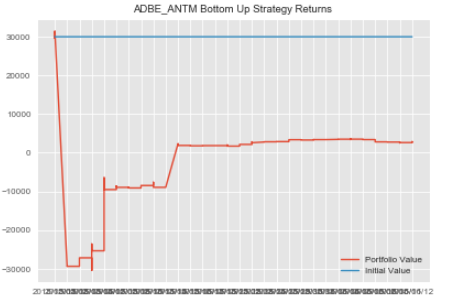

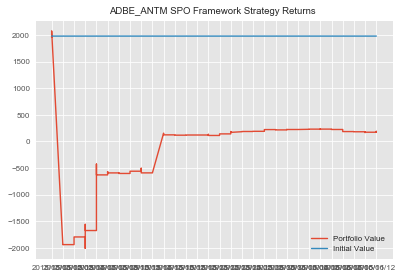

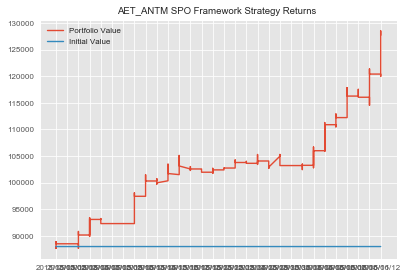

Okay! We're ready to apply our StatArb class to create our strategies. Recall that our pairs are ADBE & ANTM, ANTM & AET and AET & ANTM.

You may be wondering why we're using ANTM & AET and AET & ANTM. This is because though both pairs use the same symbols, they are in fact two completely different relationships.

In the first pair, ANTM is the X and AET is the Y. In a sense, we're asking what degree of variation in AET can be explained by a unit change in ANTM.

In contrast, in the AET & ANTM pair, we're asking what degree of variation in ANTM can be explained by a unit change in AET.

When we compute the slope or derivative, we get two completely different numbers, and thus two different relationships.

Let's now apply our StatArb class to our first pair.

#ADBE & ANTM statarb initialization #passing in X, Y, MA, Floor, Ceiling, Beta Lookback, Start, End adbe_antm=statarb(adbe_test_price_series,antm_test_price_series,17,-2,2,17,adbe_test.iloc[0],adbe_test.iloc[-1])

Let's now create our spread and generate our signals.

#creating spread adbe_antm.create_spread()

| X | Y | Beta | Spread | |

|---|---|---|---|---|

| 0 | 220.88 | 236.05 | -0.763772 | NaN |

| 1 | 220.09 | 236.74 | -0.763772 | NaN |

| 2 | 219.64 | 237.11 | -0.763772 | NaN |

| 3 | 220.34 | 237.26 | -0.763772 | NaN |

| 4 | 220.51 | 236.76 | -0.763772 | NaN |

We can now generate our signals and compute our returns on our allocation of $30k USD.

#generating signals adbe_antm.generate_signals()

#creating returns and passing in our allocation amount adbe_antm.create_returns(30000,'ADBE_ANTM')

We can repeat this process for our remaining pairs. Note, our create_spread method returned the head of our dataframe containing our spread.

We used a lookback of 17 which explains why those values are NaNs.

#repeating process for ANTM and AET antm_aet=statarb(antm_test_price_series,aet_test_price_series,6,-2,2,6,antm_test.iloc[0],antm_test.iloc[-1]) antm_aet.create_spread() antm_aet.generate_signals() antm_aet.create_returns(30000,'ANTM & AET')

#repeating process for ANTM and AET antm_aet=statarb(antm_test_price_series,aet_test_price_series,6,-2,2,6,antm_test.iloc[0],antm_test.iloc[-1]) antm_aet.create_spread() antm_aet.generate_signals() antm_aet.create_returns(30000,'ANTM & AET')

Okay. Not that we have created our individual StatArb implementations, we can combine these into a portfolio, calculate our portfolio returns, mu, sigma, and Sharpe ratio.

Note, to compute the Sharpe we will need to make an assumption about the level of interest rates.

In as of December 2017, the fed funds rate was 1.5%. We'll use this as our interest rate assumption. Recall that we started with a portfolio value of 100k USD.

We allocated 10k USD to cash and equally weighted our StatArb strategies.

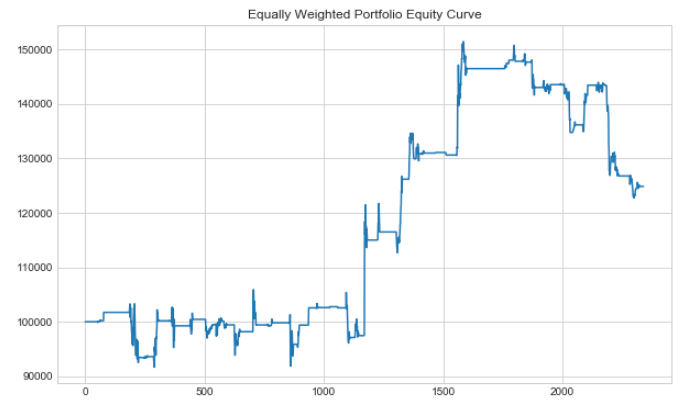

Creating the Equally Weighted Portfolio

We included a portfolio value variable in our statarb class. We'll use this to create our total equally weighted portfolio.

#creating dataframe for equally weighted portfolio equally_weighted=pd.DataFrame() equally_weighted['ADBE_ANTM']=adbe_antm.portfolio['Portfolio Value'] equally_weighted['ANTM_AET']=antm_aet.portfolio['Portfolio Value'] equally_weighted['AET_ANTM']=aet_antm.portfolio['Portfolio Value'] equally_weighted['Cash']=10000 equally_weighted['Total Portfolio Value']=equally_weighted['ADBE_ANTM']+equally_weighted['ANTM_AET']+equally_weighted['AET_ANTM']+equally_weighted['Cash']

Let's check our equally_weighted portfolio dataframe.

equally_weighted.head()

| ADBE_ANTM | ANTM_AET | AET_ANTM | Cash | Total Portfolio Value | |

|---|---|---|---|---|---|

| 0 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 |

| 1 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 |

| 2 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 |

| 3 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 |

| 4 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 |

We can now add our returns column and then use it to compute our Mu, Sigma and Sharpe ratio.

#adding returns column equally_weighted['Returns']=np.log(equally_weighted['Total Portfolio Value']/equally_weighted['Total Portfolio Value'].shift(1)) #rechecking our dataframe equally_weighted.head()

| ADBE_ANTM | ANTM_AET | AET_ANTM | Cash | Total Portfolio Value | Returns | |

|---|---|---|---|---|---|---|

| 0 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 | NaN |

| 1 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 | 0.0 |

| 2 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 | 0.0 |

| 3 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 | 0.0 |

| 4 | 30000.0 | 30000.0 | 30000.0 | 10000 | 100000.0 | 0.0 |

We'll now get our Mu, Sigma, and Sharpe and store them in variables.

#initializing Equally_Weighted portfolio metrics equally_weighted_mu=equally_weighted['Returns'].mean() equally_weighted_sigma=equally_weighted['Returns'].std() #initializing interest rate assumption of 1.5% rate=0.015 #computing Sharpe equally_weighted_Sharpe=round((equally_weighted_mu-rate)/equally_weighted_sigma,2)

Okay, let's check the Sharpe Ratio of our Equally Weighted Portfolio.

#getting Equally Weighted Portfolio Sharpe

print('Equally Weighted Portfolio Sharpe:',equally_weighted_Sharpe)Equally Weighted Portfolio Sharpe: -2.1

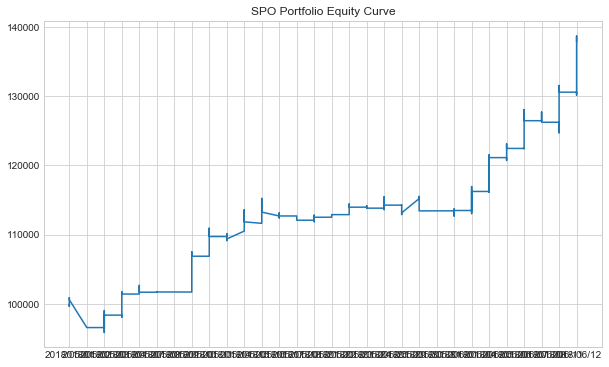

Let's plot our portfolio equity curve.

#plotting Equally Weighted Equity Curve

plt.figure(figsize=(10,6))

plt.plot(equally_weighted['Total Portfolio Value'])

plt.title('Equally Weighted Portfolio Equity Curve')

plt.show()

We can see that even though our equally weighted portfolio value increased, it still had a negative Sharpe.

We can repeat this process for our remaining portfolios and compare our Sharpe ratios.

Portfolio Construction: Efficient Frontier

Thus far we've created our Equally Weighted Portfolio and checked our Sharpe Ratio and Equity Curve.

We are now interested in what our Sharpe might be if we found the optimal weights for each of our StatArb implementations as well as the resulting effect on our equity curve.

We will now turn our attention to simulating our portfolio's mean and variance by assigning random weights to each of our pairs. We will store our portfolio's mean return and sigma and create a scatter plot that will aid us in selecting the most efficient weights for each of our strategy implementations.

To best decipher how we should weight our strategy implementations we will include logic that computes the Sharpe Ratios for each portfolio created. We can then create new instances of our StatArb implementations using updated allocations and survey the effects on our Sharpe Ratio and equity curve.

Though our Bottom Up Portfolio will be an extension of our Equally Weighted Portfolio in that it will only apply our machine learning concepts to the microstructure components, our Stereoscopic Portfolio Optimization (SPO) Framework will combine the weights found within this portfolio construction process and combine it with the process of constructing the Bottom Up Portfolio.

To begin, let's retrieve the MUs and Sigmas of our pairs. Recall that we created a method within the class that stores our mean and sigma.

We can use our strategy objects to retrieve these variables.

#initialzing Mus and Sigmas #ADBE & ANTM adbe_antm_mu=adbe_antm.mu adbe_antm_sigma=adbe_antm.sigma #ANTM & AET antm_aet_mu=antm_aet.mu antm_aet_sigma=antm_aet.sigma #AET & ANTM aet_antm_mu=aet_antm.mu aet_antm_sigma=aet_antm.sigma

The return of our portfolio can be expressed as

or as

where,

wi is the weight of the ith asset, and

ri is the return of the ith asset.

Let's create a method to compute returns.

#computing log returns for our portfolio values returns=np.log(equally_weighted[['ADBE_ANTM','ANTM_AET','AET_ANTM']]/equally_weighted[['ADBE_ANTM','ANTM_AET','AET_ANTM']].shift(1))

Let's check our returns.

#checking returns returns.head()

| ADBE_ANTM | ANTM_AET | AET_ANTM | |

|---|---|---|---|

| 0 | NaN | NaN | NaN |

| 1 | 0.0 | 0.0 | 0.0 |

| 2 | 0.0 | 0.0 | 0.0 |

| 3 | 0.0 | 0.0 | 0.0 |

| 4 | 0.0 | 0.0 | 0.0 |

We can now create our mean returns an annualize them.

avg_returns_252=returns.mean()*252

Let's check our average annualized returns.

#checking average annualized returns avg_returns

[0.00045914208401620995, 3.3720231332227273e-06, 0.00016147773221808213]

The variance of our portfolio can be expressed as

where,

wi is the weight of the ith asset,

wj is the weight of the jth asset.

Now we will use our returns to create our annualized covariance matrix.

covariance_matrix=returns.cov()*252

Let's check our covariance matrix.

covariance_matrix

| ADBE_ANTM | ANTM_AET | AET_ANTM | |

|---|---|---|---|

| ADBE_ANTM | 0.156866 | 1.205435e-04 | -2.591987e-03 |

| ANTM_AET | 0.000121 | 1.834339e-05 | -1.338726e-07 |

| AET_ANTM | -0.002592 | -1.338726e-07 | 1.212121e-03 |

We can now create a variable to hold our weights for each strategy.

#assigning weights weights=np.random.random(len(returns.columns)) weights/=np.sum(weights)

#reviewing weights weights

array([ 0.22235774, 0.15788307, 0.61975919])

The following method is an adaptation from Dr. Yves J. Hilpisch's "Python for Finance".

We'll use it to plot our Efficient Frontier and find the most optimal weights for our strategies.

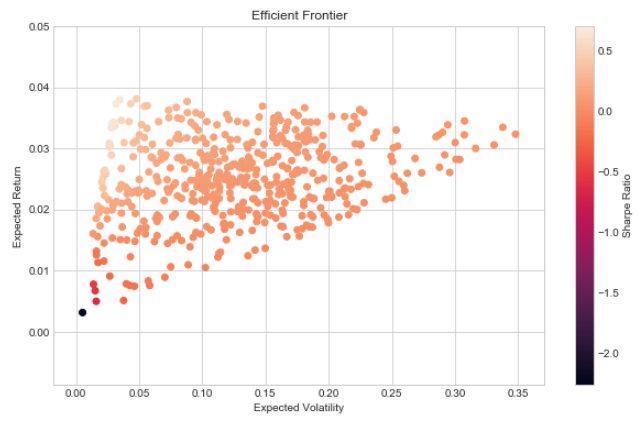

#importing optimization function import scipy.optimize as sco

def efficient_frontier(returns,rate=0.015):

#creating a list to hold our portfolio returns, variance and Sharpe values

portfolio_returns=[]

portfolio_volatility=[]

p_sharpes=[]

# returns=returns_df

for i in range(500):

#assigning weights

weights=np.random.random(len(returns.columns))

weights/=np.sum(weights)

#getting returns

current_return=np.sum(returns.mean()*weights)*252

portfolio_returns.append(current_return)

#getting variances

variance=np.dot(weights.T,np.dot(returns.cov()*252,weights))

#getting volatility

volatility=np.sqrt(variance)

portfolio_volatility.append(volatility)

#getting Sharpe ratios

ratio=(current_return-rate)/volatility

#storing Sharpe in list

p_sharpes.append(ratio)

p_returns=np.array(portfolio_returns)

p_volatility=np.array(portfolio_volatility)

p_sharpes=np.array(p_sharpes)

#plotting

plt.figure(figsize=(10,6))

plt.scatter(p_volatility,p_returns,c=p_sharpes, marker='o')

plt.xlabel('Expected Volatility')

plt.ylabel('Expected Return')

plt.title('Efficient Frontier')

plt.colorbar(label='Sharpe Ratio')

plt.show()

returnefficient_frontier(returns.fillna(0))

def stats(weights,rate=0.015): weights=np.array(weights) p_returns=np.sum(returns.mean()*weights)*252 p_volatility=np.sqrt(np.dot(weights.T,np.dot(returns.cov()*252,weights))) p_sharpe=(p_returns-rate)/p_volatility return np.array([p_returns,p_volatility,p_sharpe])

#testing stats method stats(weights)

array([ 0.0325289 , 0.08669494, 0.20219057])

#creating function for optimization def minimize_func(weights): return -stats(weights)[2]

#testing optimization function minimize_func(weights)

-0.20219056844039546

def get_optimal_weights(weights):

#Finding Most Optimal Weights

#variables for optimization

constraints=({'type':'eq','fun':lambda x: np.sum(x)-1})

bounds=tuple((0,1) for x in range(len(returns.columns)))

starting_weights=len(returns.columns)*[1./len(returns.columns)]

most_optimal=sco.minimize(minimize_func,starting_weights, method='SLSQP', bounds=bounds, constraints=constraints)

best_weights=most_optimal['x'].round(3)

return best_weights, print('Weights:',best_weights)#storing optimal weights in a variable optimal_weights=get_optimal_weights(weights)

Weights: [ 0.022 0. 0.978]

Okay. We can see that the most optimal weights are to allocate 2% of our capital to ADBE_ANTM, 0% to ANTM_AET and 97.8% to AET_ANTM.

Recall that our method was designed to optimize our Sharpe ratio. We can now implement another instance of our strategies using these weights and create our portfolio and compute its equity curve.

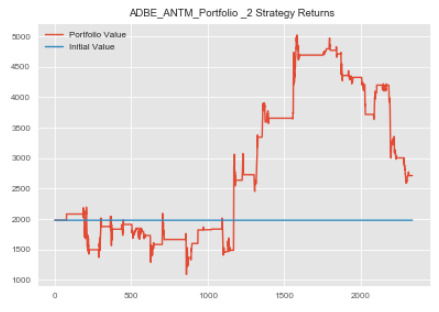

Let's create our second instance of the ADBE_ANTM pair.

We'll create a total_allocation variable that we can use to compute our allocation to our strategies.

#total allocation variable total_allocation=90000 #100k less 10k cash #ADBE_ANTM Allocation adbe_antm_allocation=round(total_allocation*optimal_weights[0][0],2) #AET_ANTM Allocation aet_antm_allocation=round(total_allocation*optimal_weights[0][2],2)

#creating 2nd instance of first pair adbe_antm_2=statarb(adbe_test_price_series,antm_test_price_series,17,-2,2,17,adbe_test.iloc[0],adbe_test.iloc[-1]) adbe_antm_2.create_spread() adbe_antm_2.generate_signals() #notice here we're using our updated allocation adbe_antm_2.create_returns(adbe_antm_allocation,'ADBE_ANTM_Portfolio _2')

Recall that our second pair received a 0% allocation. We will thus create our 3rd pair with the updated weight and create our new portfolio.

#AET_ANTM 2nd implementation aet_antm_2=statarb(aet_test_price_series,antm_test_price_series,12,-2,2,12,aet_test.iloc[0],aet_test.iloc[-1]) aet_antm_2.create_spread() aet_antm_2.generate_signals() aet_antm_2.create_returns(aet_antm_allocation,'AET & ANTM')

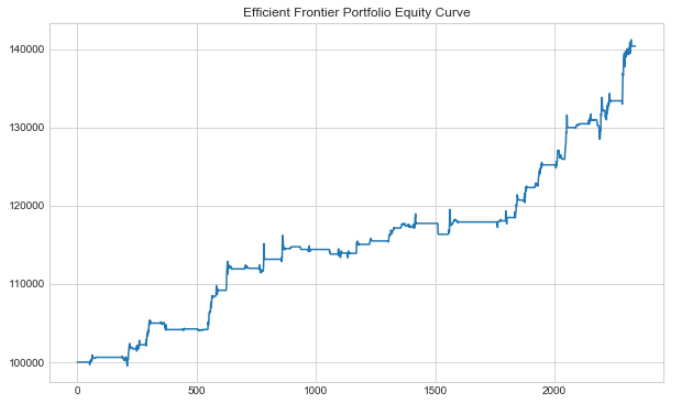

We are now ready to compose our Efficient Frontier Portfolio.

Creating the Efficient Frontier Portfolio

Let's create our Efficient Frontier Portfolio.

#creating dataframe for Efficient Frontier Portfolio efficient_frontier_portfolio=pd.DataFrame() efficient_frontier_portfolio['ADBE_ANTM']=adbe_antm_2.portfolio['Portfolio Value'] efficient_frontier_portfolio['AET_ANTM']=aet_antm_2.portfolio['Portfolio Value'] efficient_frontier_portfolio['Cash']=10000 efficient_frontier_portfolio['Total Portfolio Value']=efficient_frontier_portfolio['ADBE_ANTM']+efficient_frontier_portfolio['AET_ANTM']+efficient_frontier_portfolio['Cash']

We can now add our returns column to our Efficient Frontier Dataframe.

#adding returns column to Efficient Frontier Dataframe efficient_frontier_portfolio['Returns']=np.log(efficient_frontier_portfolio['Total Portfolio Value']/efficient_frontier_portfolio['Total Portfolio Value'].shift(1))

We can now check our Efficient Frontier Portfolio Dataframe.

#checking head of Efficient Frontier Portfolio dataframe efficient_frontier_portfolio.head()

| ADBE_ANTM | AET_ANTM | Cash | Total Portfolio Value | Returns | |

|---|---|---|---|---|---|

| 0 | 1980.0 | 88020.0 | 10000 | 100000.0 | NaN |

| 1 | 1980.0 | 88020.0 | 10000 | 100000.0 | 0.0 |

| 2 | 1980.0 | 88020.0 | 10000 | 100000.0 | 0.0 |

| 3 | 1980.0 | 88020.0 | 10000 | 100000.0 | 0.0 |

| 4 | 1980.0 | 88020.0 | 10000 | 100000.0 | 0.0 |

We'll now plot the equity curve for our Efficient Frontier Portfolio.

#plotting Equity Curve for Efficient Frontier Portfolio

plt.figure(figsize=(10,6))

plt.plot(efficient_frontier_portfolio['Total Portfolio Value'])

plt.title('Efficient Frontier Portfolio Equity Curve')

plt.show()

We can now store our Mu, Sigma, and Sharpe for our Efficient Frontier Portfolio in variables.

efficient_frontier_portfolio_mu=efficient_frontier_portfolio['Returns'].mean() efficient_frontier_portfolio_sigma=efficient_frontier_portfolio['Returns'].std() #recall that we initialized our interest assumption earlier efficient_frontier_portfolio_sharpe=(efficient_frontier_portfolio_mu-rate)/efficient_frontier_portfolio_sigma

Okay. We've just finished our second portfolio. Two down and two to go.

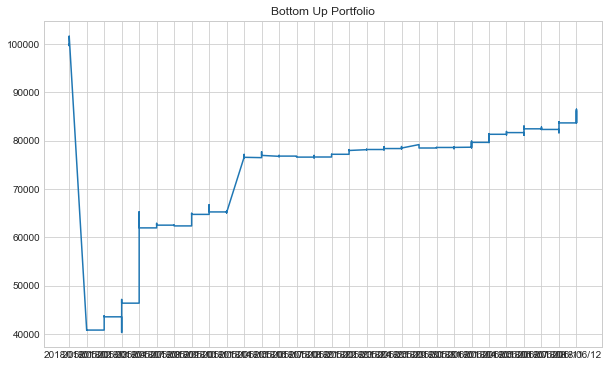

We can now begin constructing our Bottom Up Optimization Portfolio.

Portfolio Construction: Bottom Up Optimization

The Bottom Up Portfolio applies machine learning to the composition of the equally weighted portfolio.

This means that we will use equal weights but instead of optimizing using the Efficient Frontier, we will use bottom-up optimization.

- The idea is to have our GMM identify specific regimes or distributions.

- We can then use our GMM's predictions as labels for our Random Forests.

- Our signal generator will then trade based only when our strategy is within a regime in which it historically has not underperformed.

Recall that our assessment period is from 5/1/18 to 6/12/18. In our prior portfolios, we were able to create our portfolios using this period.

In this portfolio, however, we will be using machine learning. That means that we will need to create our models over the period beginning 1/4/18 and ending 4/30/18 and actually construct on portfolio using these models over our test period.

Let's begin by creating our training period variables.

Recall that we created a dataframe earlier called training_df that held our data over our training period.

We initially created this dataframe so that we could test for cointegration over our training period. We can now reuse it here.

Let's review our training_df dataframe.

training_df.head()

| ADBE | AET | AIG | ANTM | AMAT | |

|---|---|---|---|---|---|

| 0 | 183.13 | 183.45 | 60.36 | 229.62 | 54.67 |

| 1 | 182.89 | 183.68 | 60.61 | 229.63 | 54.51 |

| 2 | 183.22 | 183.80 | 60.77 | 229.70 | 54.25 |

| 3 | 183.73 | 183.82 | 60.81 | 229.65 | 54.08 |

| 4 | 183.90 | 183.93 | 60.80 | 229.70 | 54.27 |

We have the prices of our symbols from 1/4/18 to 4/30/18. No pair containing AMAT was found to be cointegrated at least 90% confidence interval so we won't be using it.

We can now recreate our equally weighted strategy implementations using our training period data.

Once we have the returns for our implementations we can then engineer some features to use in training our Gaussian Mixture Model. We will then use these predictions as labels for our Random Forests.

Once we've trained our Random Forests to predict the regimes found by our Gaussian Mixture Model, we can then use those predictions to augment our signal generator, avoiding troublesome regimes.

Let's begin creating our strategy implementations.

Step 1: Feature Engineering

We are now ready to engineer our features. In order to predict what regime our strategy is in based on its historical performance, we will need features or explanatory variables.

Market-Microstructure encompasses a vast array of components including liquidity, volatility, market depth, etc. For this illustration, we will use volatility.

We will track the volatility of each of our underlying components, our spread, and our z-score.

These features will be used within our Random Forests to predict the regimes identified by our Gaussian Mixture Model.

Step 2: Creating Strategies Over Historical Period

We'll begin with our first pair, ADBE_ANTM. Before we begin our implementation we need to split our historical period.

Recall that we imported intraday data from 1/4/18 to 6/12/18. Our assessment period or the period in which we are comparing our Sharpe ratios is from 5/1/18 to 6/12/18. In our first two portfolios, we simply applied our strategies to our assessment period.

However, in our later two portfolios, we need to first apply it to our historical period to train our models then apply it to our assessment period.

To assess our models before applying them to our true testing or assessment period we need to split our historical period into a historical training and testing set.

This will enable us to train our models on part of our total training data and then test it on our historical testing data. We can then apply them to our overall testing or assessment period.

For simplicity, we'll manually calculate an 80/20 train_test_split.

#checking length of training_df len(training_df)

6240

#computing 80% of training_df length len(training_df)*.80

4992.0

#computing 20% of training_df length len(training_df)*-.20

-1248.0

Okay now that we have the index values that represent the 80% and 20% marks of our training_df dataframe, we can use them to slice our data.

The way that we can do this is for our 80%, or the first 4992 rows we can simply use the notation [0:4992]. For our testing period over our historical training period, we can parse the last 20% by using the notation [-1248].

These notations will be used to split the returns we generate over our entire historical period.

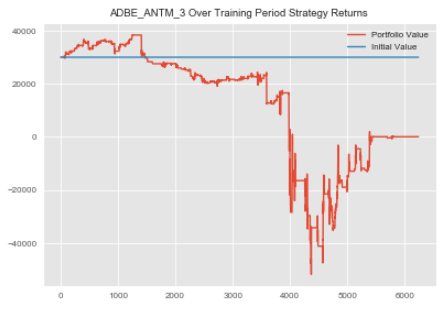

Let's create our ADBE_ANTM implementation.

adbe_antm_3_historical=statarb(training_df['ADBE'],training_df['ANTM'],17,-2,2,17,adbe_test.iloc[0],adbe_test.iloc[-1]) adbe_antm_3_historical.create_spread() adbe_antm_3_historical.generate_signals() #notice that we are equally weighing our strategy adbe_antm_3_historical.create_returns(30000,'ADBE_ANTM_3 Over Training Period')

Okay now that we've created our strategy, let's check our returns.

adbe_antm_3_historical_rets=adbe_antm_3_historical.portfolio['Returns']

#checking head of returns adbe_antm_3_historical_rets.head()

0 1.0 1 1.0 2 1.0 3 1.0 4 1.0 Name: Returns, dtype: float64

We will now repeat this process for our remaining pairs.

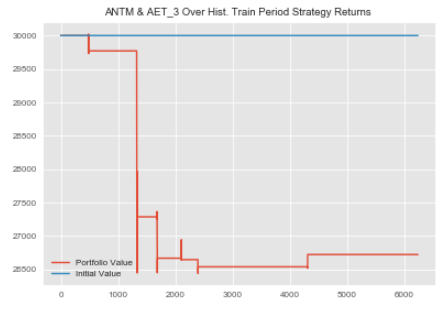

#ANTM_AET Bottom Up Historical Implementation antm_aet_3_historical=statarb(training_df['ANTM'],training_df['AET'],6,-2,2,6,antm_test.iloc[0],antm_test.iloc[-1]) antm_aet_3_historical.create_spread() antm_aet_3_historical.generate_signals() antm_aet_3_historical.create_returns(30000,'ANTM & AET_3 Over Hist. Train Period')

Let's store our returns from the ANTM_AET training period in a variable

antm_aet_3_historical_rets=antm_aet_3_historical.portfolio['Returns']

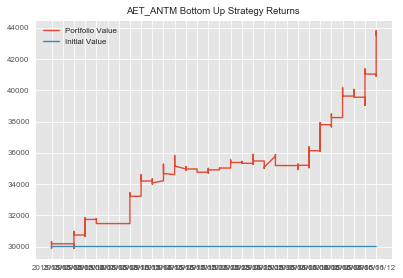

Okay, now we finish up with our AET_ANTM pair.

aet_antm_3_historical=statarb(training_df['AET'],training_df['ANTM'],12,-2,2,12,aet_test.iloc[0],aet_test.iloc[-1]) aet_antm_3_historical.create_spread() aet_antm_3_historical.generate_signals() aet_antm_3_historical.create_returns(30000,'AET & ANTM')

aet_antm_3_historical_rets=aet_antm_3_historical.portfolio['Returns']

#checking AET_ANTM returns over the training period aet_antm_3_historical_rets.head()

0 1.0 1 1.0 2 1.0 3 1.0 4 1.0 Name: Returns, dtype: float64

Step 3: Using Gaussian Mixture Model to Identify Historical Regimes

We now have the returns of our StatArb strategies over our historical period.

Our next task is to identify our historical regimes. Our goal is to identify the regimes in which our stratetgies have not performed well on a risk to reward basis and avoid these periods.

To achieve this, we must:

- identify our historical regimes and

- engineer features that can be used to predict these regimes.

We can then augment our signal generator and thus optimize our portfolio from the microstructure level up.

We'll begin by splitting our returns data into an 80/20 train test split.

#splitting historical returns data #ADBE_ANTM #getting length of returns data adbe_antm_3_rets_len=len(adbe_antm_3_historical_rets) adbe_antm_3_rets_train=adbe_antm_3_historical_rets[0:4992] adbe_antm_3_rets_test=adbe_antm_3_historical_rets[-1248:] #ANTM_AET #getting length of returns data antm_aet_3_rets_len=len(antm_aet_3_historical_rets) antm_aet_3_rets_train=antm_aet_3_historical_rets[0:4992] antm_aet_3_rets_test=antm_aet_3_historical_rets[-1248:] #AET_ANTM #getting length of returns data aet_antm_3_rets_len=len(aet_antm_3_historical_rets) aet_antm_3_rets_train=aet_antm_3_historical_rets[0:4992] aet_antm_3_rets_test=aet_antm_3_historical_rets[-1248:]

Now that we have created our train and test splits we're ready to identify our regimes. We'll start by training our GMM on our training period data, then we'll apply it to our testing period data.

We'll create a method that we can use for our GMM and Random Forests.

class gmm_randomForests(object):

def __init__(self,historical_rets_train,historical_rets_test,base_portfolio_rets,gmm_components,df,base_portfolio_df,

internal_test_start,internal_test_end):

'''

PARAMETERS

##########

The first 3 parameters should have already been sliced from the

entire sample; ie specific dates parsed from dataframe that contains

trade history, returns, and features; other features will be added

later in development within the object

historical_rets_train- the returns data over the historical period used to train on

this is the internal train of the internal 80/20 split;the 80%

of the total historical training set

historical_rets_test- retuns data for 20% of internal training test set

base_portfolio_rets - this is our figurative live data;ie returns; 5/01/18-6/12/18 from either

Equally Weighted or Efficient Frontier Portfolios dependent upon implementation

of Bottom Up or Stereoscopic Portfolio Optimization (SPO) Framework

ex. data over 01/04/18-04/30/18

we would first split this 80/20

the 80% is our training set

the 20% is our testing set

we would then do another split on our training set created above

this is so that if we can better understand the historical

regimes and recalibrate our models if necessary before actually

predicting our 5/1/18-6/12/18 testing set

in this ex. our gmm_training_train is 80% of the period 01/04/18-4/30/18

our gmm_training_test is 20% of the period 01/04/18-4/30/18 and our

gmm_test_actual is 05/01/18-6/12/18

gmm_components - type:int; for number of components for GMM

df - the entire dataframe containing prior trading history; the dataframe from either Equally Weighted or

Efficient Frontier Portfolios; Our Random Forests Implementation will take this dataframe created by

our statarb class(i.e. from the prior portfolios) and add our features to it. It will then use these

features to predict the regimes of our test period. Recall that our Equally Weighted and Efficient

Frontier Portfolios were constructed over our assessment period of 5/1/18 to 6/12/18. We will then

be able to store our predictions in a varible for our test period. These predictions will be passed

into a new statarb object as a parameter and be used to create the Bottom Up and SPO Framework Portfolios.

total_training_start- type: string; the beginning of the historical period for analysis; input as string

from example above would be 2012

total_training_end - type:string; the end of the historical period for analysis; input as string;

from example above would be 2017

base_portfolio_df - (i.e.adbe_antm.df,etc)Note: for the Bottom Up Implementation this df would be the Equally Weighted df but for the

SPO Framework df this would be the df from the Efficient Frontier implementation

internal_test_start- type:int; this is the testing period for the total training period; in the example,

this is the assessment period of 05/01/18-06/12/18; start thus is len(strategy_object)*.80

internal_test_end - type:int; this is the end of the assessment period; ie. the 20% testing split

of the broader split...this value is -len(strategy_object)*.20...Note this value is

is negative because we want the last 20% of the data

The last two methods are created as such because our Equally Weighted and Efficient Frontier

Portfolios are not indexed by dates but are indexed by a sequence of ints. This means

that in a later method(i.e. Random Forests) we have to pass in the int value of the index

position we want to parse

'''

self.historical_rets_train=historical_rets_train

self.historical_rets_test=historical_rets_test

self.base_portfolio_rets=base_portfolio_rets

self.gmm_components=gmm_components

self.max_iter=300

self.random_state=101

self.df=df

#self.total_training_start=total_training_start

#self.total_training_end=total_training_end

self.base_portfolio_df=base_portfolio_df

self.internal_test_start=internal_test_start

self.internal_test_end=internal_test_end

#creating volatility

self.volatility=self.historical_rets_train.rolling(window=5).std()

self.negative_volatility=np.where(self.historical_rets_train<0,self.historical_rets_train.rolling(window=5).std(),0)

def make_gmm(self):

model_kwds=dict(n_components=self.gmm_components,max_iter=self.max_iter,n_init=100,random_state=self.random_state)

gmm=GM(**model_kwds)

return gmm

def analyze_historical_regimes(self):

#Creating a Gaussian Mixture Model

self.gmm=self.make_gmm()

#instantiating the XTrain as the gmm_training_train; (i.e. the 80% of total training period)

self.gmm_XTrain=np.array(self.historical_rets_train).reshape(-1,1)